By John Helmer, Moscow

United Company Rusal has admitted that one large international bank is refusing to accept the restructuring terms the company has offered for loans totaling $5.15 billion which fall due for repayment by July 7. Until now, there has been speculation that state-owned Chinese banks had been pressing for repayment in cash, rather than accept extension of the loan maturity date and other terms. On Friday, the holdout banks were identified by Rusal sources as Royal Bank of Scotland (RBS), which is majority-owned by the UK Government; and the German bank WestLB, which has been in a form of bankruptcy management since June 2012. Today, Portligon, which has taken over WestLB, reportedly changed its mind, and accepted Rusal’s offer of terms.

The latest Rusal disclosures also provide for an international court to oblige the last holdout to accept another four to five months of negotiating time, thereby preventing it from pitching Rusal into default and bankruptcy next Monday.

A Rusal notice to the Hong Kong Stock Exchange last Friday (June 28) revealed that “as of today’s date, 94 percent of Lenders have expressed support for the Amendment agreement. The Company is continuing to seek the support of the six percent of Lenders which have not already done so.” The holdouts were identified to Bloomberg and the Financial Times by Oleg Mukhamedshin, Rusal’s deputy chief executive , and “two people with knowledge of the situation”.

At stake is Rusal’s solvency. The financial report for the March quarter shows a bottom-line loss of $325 million; the loss for 2013 was $3.32 billion. As of March 31, liabilities were between $$11.5 billion and $13.9 billion. Cash on hand was reported as $537 million, slipping away at a rate of $55 million per month. According to KPMG’s latest audit report warning, issued on May 12, “there is significant uncertainty as to whether the Group will have sufficient cash flows to meet its scheduled debt repayments falling due during 2014 unless a debt restructuring is cornpleted that both defers principal repayments to future periods and rnodifies financial covenants to sustainable levels. In the event the Group is unable to reach an acceptable agreement to restructure its scheduled debt repayments and related financial covenants…[there is] material uncertainty that may cast significant doubt about the Group’s ability to continue as a going concern.”

Rusal claimed Friday there has been “significant further progress in obtaining the support of the PXF [pre-export finance] lenders.” Either the number of banks vetoing the reorganization of Rusal’s debt has been multiplying; or Rusal and Bloomberg have been misleading the market. On March 31, Rusal sources told Bloomberg: “the one holdout is a small institution in Europe…declining to identify it.”

Mukhamedshin (right) claimed on Friday the two banks were “seeking an unjustified premium for the debt they hold.” Today Rusal refused to say what amounts the company currently owes RBS and WestLB, and what “premium” the Rusal executive was referring to.

Mukhamedshin (right) claimed on Friday the two banks were “seeking an unjustified premium for the debt they hold.” Today Rusal refused to say what amounts the company currently owes RBS and WestLB, and what “premium” the Rusal executive was referring to.

Russian reports have estimated that RBS, along with the French banks Natixis and BNP Paribas, are collectively owed $350 million. Bank sources believe RBS and WestLB may be owed more than this. Rusal sources refuse to clarify the precise amount.

There has been speculation in the market that because of the stance the British Government has taken in favour of tough Ukraine-related sanctions against Russia, RBS – 64% owned by the government – has been under pressure to demand full cash repayment without further delay. US Government officials have also been reported by London sources as quietly urging RBS, as well as other international banks with Russian refinancings in negotiation, not to lend to Russian corporate clients. For the story of these “stealth sanctions”, read this.

Mukhamedshin has told reporters the sanctions campaign is not involved. He also minimized the amount of money the holdouts are owed. “We are not talking about a big amount… it’s pure commercial stuff,” he told the Financial Times.

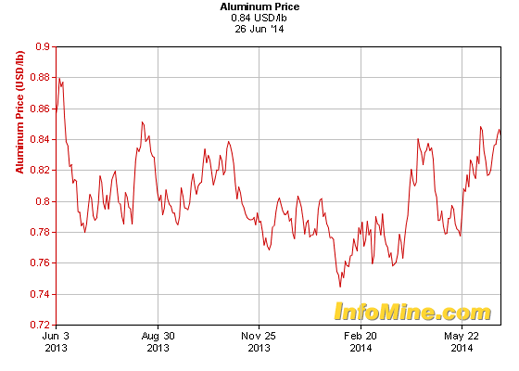

An international banker who has negotiated with Rusal already over the restructuring of these loans said Rusal has attempted to link its repayment obligations to the price of aluminium on the London Metal Exchange (LME). “There are many ways a bank can bet on the price of aluminium, if it wants, but noone wants to do that through Rusal.” The chart showing the aluminium price lower now than it was a year ago explains why:

Source: http://www.infomine.com/

Another source familiar with the term sheet for the negotiations between Rusal and the international banks, says Rusal is asking for a grace period of two further years to 2016 before required repayments will recommence, unless the aluminium price rises by enough to lift Rusal’s cashflow. Improvement in Rusal’s takings from its stake in Norilsk Nickel has been promised, plus further reductions of debt by a selloff of Rusal assets. One of the assets promised for sale is the Aluminium Smelter Company of Nigeria (ALSCON). For the time being, that asset is more likely to add to Rusal’s liabilities than to reduction of its debts. Click for more.

Rusal’s notice to the Hong Kong Exchange also threatens the banks, which have already accepted a postponement of repayment and other terms, with the possibility of protracted legal action to keep everyone in line. “As of today’s date”, Rusal claimed Friday, “94 percent of Lenders have expressed support for the Amendment Agreement. The Company is continuing to seek the support of the six percent of Lenders which have not already done so. In the meantime, however, in the absence of unanimous Lender support, and with the support of the coordinating banks, the Company is proposing to apply to the courts in England and Jersey to pursue a scheme of arrangement… to implement the Amendment Agreement. In order to be approved by the courts, the Scheme of Arrangement will require the support of at least 75 percent by value and a majority in number of the relevant classes of Lenders.”

A filing in the UK High Court is scheduled for July 10, and another filing in the Royal Court of Jersey on July 15. An international lawyer with experience of this type of litigation says “a solvency scheme of arrangement for a particular class of creditors under UK law requires a 75% majority per class of creditor, plus court sanction. The procedure ought to take a minimum of half a year. The courts are getting increasingly restrictive. There are also considerable legal fees.”

An international banker says Rusal’s court application is a bluff. An application to the Jersey court, where Rusal is registered, is unlikely to persuade any of the banks, the source believes, because Rusal conducts no significant business there, and a Jersey court order would lack the required legal force to compel the banks holding out against Rusal’s terms. “It is highly unlikely that an offshore centre [Jersey] can force a holdout [to accept terms].”

Other sources say that RBS is unlikely to want to add to the costs of its Rusal exposure by coming into court, either in London or St. Helier, to defend the right to seek cash repayment now. While the UK has strict rules on what holdout lenders in a loan syndicate can be compelled to accept, over their objections, lawyers believe the least Rusal can achieve now is another four months of “forbearance” for negotiations, maybe longer; that is, “the period of time starting on the effective date of the Lock-Up Agreement [July 1] and ending on the earlier of (a) 31 October 2014 or such later date as might be agreed, provided such date is not later than 30 November 2014; (b) the date on which the amendments sought under the Amendment Agreement become effective.”

If there is political pressure from the US Treasury to block the refinancing, the banks are not willing to say so. A UK court ruling would, however, shield RBS from the sanctions pressure, as the UK and European Union courts have already ruled that political sanctions are unlawful unless they are demonstrably relevant and proportional to cause and purpose. See If the UK and Jersey courts take six months to rule on Rusal application, the shield effect would be similar.

Rusal has also tried to persuade the foreign banks that it will reduce its bottom-line loss-making by guaranteeing with Norilsk Nickel the payment of dividends equal to 50% of Norilsk Nickel earnings, but not less than $2 billion per annum. An announcement to this effect was issued on June 26. Rusal’s entitlement under this scheme would be 27.82% of the Norilsk Nickel earnings figure (equal to its shareholding stake). For 2013 that would amount to 27.82% of $2.1 billion, or $584.2 million. So far, Rusal and its auditors are recording its share of the profit from continuing Norilsk Nickel operations of just $105 million for 2013; $77 million for the first quarter of 2014.

Leave a Reply