By John Helmer, Moscow

@bears_with

The Russian regime-change theory motivating US sanctions against the Russian oligarchs is that they will trigger a palace coup in which the oligarchs will arrange a bullet for President Vladimir Putin’s head, and in return the US will give them back the keys to their yachts, mansions, and offshore bank accounts.

The terms of pain relief and life insurance which the oligarchs are discussing with Putin are different. The oligarchs want to be compensated for what they have lost offshore with an even larger stock of assets onshore, including takeover of exiting foreign companies and privatization of state assets; low-interest Central Bank finance; import substitution and labour subsidies; tax holidays; postponement of ecological compliance; deregulation; amnesty for past crimes, immunity from prosecution for future ones.

Secret though the details of their agreement are – must be in time of war – the new shape of the oligarchs’ wealth can begin to be gauged from an initial inventory. As for the new policy pact directing it, it is easier to say what it is not — it bears no resemblance to the recommendations for nationalization, state planning, ban on foreign investment in hostile states, a high ruble rate to protect against imports, and de-dollarization for exports, which have been proposed by the former Kremlin economic adviser, Sergei Glazyev.

When President Vladimir Putin announced at his meeting with state officials on May 24, that he proposes “red tape needs to be scrapped” and “additional adjustments to the regulatory framework”, the phrases were not new. In the war economy, however, they signal deregulation and privatization — more freedom for the oligarchs, not less. When Putin added: “the Russian economy will certainly remain open in the new conditions”, the meaning, at least as the oligarchs are interpreting it, is that the president is promising more freedom from the state, not less.

Glazyev (61) is the best known government official in Moscow opposing this line, and proposing instead a fully fledged alternative strategy. Glazyev, a trade minister during the first Yeltsin administration; a member of the anti-Yeltsin coalition of 1996 led by Alexander Lebed and Dmitry Rogozin; for many years that followed Glazyev was an official economic adviser to Putin. Currently, he is minister for integration and macroeconomics of the Eurasian Economic Commission (EEC, aka EAEU ), the bloc of former Soviet states coordinating customs, central banking, trade and fiscal management policies together.

In March Glazyev led the public campaign to replace Elvira Nabiullina (58) as the governor of the Central Bank; Putin decided against Glazyev for Nabiullina. Follow the archive here.

Glazyev isn’t alone; he is associated with the Anti-Crisis Expert Council which includes the public economist Mikhail Khasin (60) and Duma deputy Mikhail Delyagin (54). Glazyev’s website can be followed here; Khasin here; and Delyagin here. Glazyev and Delyagin, who is chairman of the Duma Committee on Economic Policy, have been sanctioned officially by the US Treasury; Khasin has been targeted but not sanctioned.

Left to right: Sergei Glazyev, Foreign Minister Sergei Lavrov, President Putin; Mikhail Khasin; Mikhail Delyagin.

Nabiullina was reappointed to run the Central Bank of Russia (CBR) on March 18. Three weeks later, Glazyev published his most detailed plan yet for the war economy; it is also a comprehensive attack on everything Nabiullina stands for. In interview form on Glazyev’s website, read the original Russian text here.

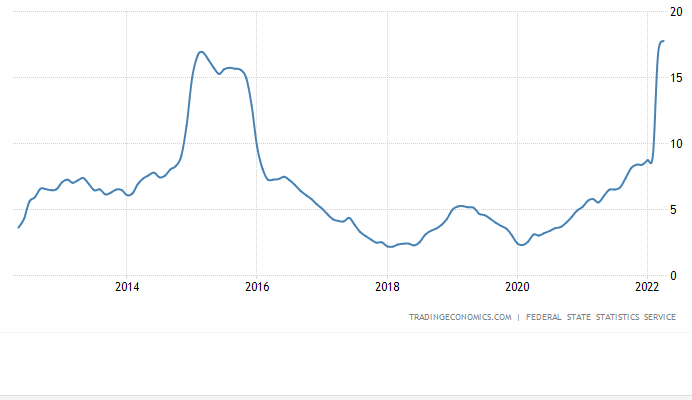

“The global crisis, which began in 2008 as a financial one, turned into a pandemic in 2020 and is now continuing as a military-political one –” declared Glazyev, “represents three phases of a global hybrid war waged by the US government and financial elite for the preservation of global dominance. As the crisis deepens, it becomes more and more aggressive in an effort to stop the development of China that has pulled ahead. At the same time, it gets mainly to Russia, which Anglo-Saxon politicians, sick with hereditary Russophobia, all want to destroy and break its strategic partnership with China. The damage from the anti-Russian sanctions imposed by the United States and the EU is collectively estimated at $1 trillion. They are aggravating the 8-year stagnation of the Russian economy caused by the ridiculous policy of the Bank of Russia. Under the guise of ‘targeting’ inflation, the Bank gave the formation of the ruble exchange rate to currency speculators and paralyzed investment activity by a sharp increase in the key interest rate. The consequence of such a policy of economic suicide was the underproduction of goods and services by almost 50 trillion rubles.”

RUSSIAN CENTRAL BANK INTEREST RATE, 2003 UNTIL NOW

“I can mathematically prove that 80% of the losses of the Russian economy — which could grow by 8% of GDP growth per year on the basis of the available resources — are explained by the policy of the Bank of Russia, and 20% by the negative impact of sanctions. I think this proportion will continue in the future if monetary policy is not radically changed in accordance with the best international practice. Meanwhile, we could develop no worse than China if we implemented the policy of advanced economic development that we have been proposing for a long time. To do this, we have all the necessary resources: production facilities loaded by barely half; labour resources capable of increasing output by 20% at full capacity utilization, and which can be increased due to the common labour market of the EEC [EAEU] and labour migration from Ukraine and Central Asia; inexhaustible volumes of raw materials which can be processed into finished products instead of exports; as well as a powerful scientific and technical potential, used by barely a third. The only thing our economy lacks is loans – they have become inaccessible to most manufacturing enterprises due to the systematic overestimation of the key rate by the Bank of Russia.”

Glazyev is particularly critical of Nabiullina’s manipulation of the CBR interest rate for the purpose, she says, of combating inflation.

RUSSIA’S ANNUAL INFLATION RATE, 2003 UNTIL NOW

“In a much worse situation after the default of 1998, the [Prime Minister Yevgeny] Primakov–[CBR Governor Viktor] Gerashchenko government managed to stabilize the macroeconomic situation within a month and launch production growth, the pace of which in industry reached 2% per month. This was achieved by a combination of stabilization of the ruble exchange rate by cutting off speculators from the foreign exchange market and expanding lending to output by enterprises which took advantage of the sharp devaluation of the ruble to produce import-substituting products. Gerashchenko did not raise the refinancing rate, which remained much lower than inflation all this time, and he fixed the currency position of commercial banks in order not to give them the opportunity to play down the ruble exchange rate.”

“Now the Bank of Russia, on the contrary, has sharply raised the key rate, and blocked the operation of the exchange, giving commercial banks the opportunity to speculate on the foreign exchange market without restraint. Thus, [the Bank] blocked the increase in credit to enterprises which could increase the output of import-substituting products, and instead allowed banks to profit from currency speculation. The government, not having sufficient opportunities to stimulate the growth of production and investment, has taken the path of deregulation of imports to the detriment of domestic producers. Instead of increasing the output of domestic products now to replace European and American goods which have left the Russian market, the bet is on filling it with substandard cheap imports from other countries.”

Dinner at the Catherine Palace, Tsarskoye Selo, St. Petersburg, June 23, 2012 (left to right): Henry Kissinger, Avdotya Smirnova (Anatoly Chubais’s wife), Anatoly Chubais, Elvira Nabiullina, Alexei Kudrin.

“Now it will be necessary to do the same as in the second half of 1998. Then, instead of the new decline in production predicted now, we should revive the growth spurt which the President of Russia is calling for.”

Glazyev’s war economy strategy calls for reducing the CBR interest rate for interbank lending to 1%, and for loans to companies to 2%, using a special state investment fund of Rb10 trillion targeted at enterprises producing import substitutes, as well as the “creation and expansion of production facilities of a new technological type based on our existing scientific and technical potential. The most obvious areas of import substitution with a colossal multiplicative effect include: civil aircraft, shipbuilding, instrumentation, energy and heavy engineering, production of oil and gas equipment, oil and gas chemistry, complex processing of timber, the food industry.” By combining investment and financing plans with the other members of the EEC (EAEU), “we can dramatically increase the production of clothing and shoes, household and computer equipment, agricultural machinery, machine tools. Western competitors are handing over the Russian market without a fight, and it’s a sin not to take advantage of it.”

To run this new economic plan, Nabiullina and the CBR should be subordinated to “full-scale strategic planning…[to] provide for subordination of macroeconomic policy, including its monetary component [CBR], to the goals of modernization and growth of production of high-tech military and dual-use products. To do this, credit lines should be organized with a rate of no more than 2% per annum for borrower enterprises to produce under government orders [procurement] and work under government programs [subsidies].”

The ownership of the assets of companies whose foreign owners have announced their exit and sale should be their nationalization, with state bank financing: “I would transfer such enterprises to labour collectives. No one else is interested in saving the jobs. But this is the main criterion that is proposed to be introduced as an obligation for those who claim to manage abandoned enterprises.”

Glazyev has long advocated the de-dollarization of Russian exports. “Our numerous proposals to transfer payments for the export of Russian energy carriers and other raw materials to rubles were met with a decisive refusal from both exporters and their lobbyists in the financial branch of government. The latter [Chubais, Kudrin, Nabiullina] frightened the political leadership with the contraction of foreign exchange reserves and the collapse of the ruble exchange rate, thus keeping the line on dollarization of our foreign trade. In combination with the abolition of the mandatory sale of foreign exchange earnings, this entailed a consistent increase in non-refundable foreign exchange earnings in offshore companies, the volume of which exceeded a trillion dollars on the eve of the ‘sanctions from hell’. The financial technocrats in our government, about whom the author of these sanctions, Daleep Singh, deputy National Security Adviser to the President of the United States for international economics, let slip the other day as agents of the United States, literally threw tantrums in response to our proposals to transfer oil and gas exports to rubles. Now the same financial technocrats are forced to hastily carry out the instructions of the President of Russia, immediately after which the ruble began to strengthen.”

Daleep Singh (right) meets Foreign Secretary Harsh Vardhan Shringla in Delhi, April 2, 2022. For the authorized New Yorker version of Daleep Singh’s role in US sanctions planning, click to read. In this piece, an unnamed source described Nabiullina as one of several “pretty solid, talented group of technocrats there”. Singh, according to the report, “flew below the radar of Russian intelligence”. Daleep claims personal credit for the US decision to seize the CBR’s foreign reserves – “it was important for us to show that the fortress could come crumbling down.” For New Delhi pushback, after Singh threatened the Indian government.

“If our monetary authorities had followed the recommendations of domestic scientists, and not the instructions of the US Treasury and the IMF,” Glazyev warns, “there would not have been such a large-scale capital drain and hundreds of billions of dollars frozen in US-controlled offshore accounts would have been invested in the Russian economy, and the ruble would have become a full-fledged world reserve currency.”

“Right now what is necessary is to make sure that they [Nabiullina, the CBR and the Finance Ministry] do not disrupt the execution of the instruction of the President on the transfer of payments for gas to rubles. If this is fulfilled, the Europeans themselves will resort to our market with their goods and euros, and the ruble will finally be quoted as a fully fledged currency; direct quotations of the ruble and yuan, ruble and rupee will begin on the Moscow stock exchange; a fully fledged market for settlements in national currencies with our main partners will be created, in which the ruble will take its proper place as one of the reserve currencies. And it will no longer be possible to steal foreign exchange earnings undetected through cut-out companies.”

Read more on what Glazyev calls the “gasket” mechanism for capital diversion offshore.

“In addition to paying for gas in rubles, the sanctioning countries should be obliged to pay for importing our energy, metals, fertilizers, timber, and grain exclusively in ‘hard’ currencies — the ruble, yuan, physical gold. To do this, the Bank of Russia needs to ensure the stability of the ruble by regulating its supply for foreign trade operations in accordance with the trade and balance of payments. A possible option is to return to the model of a ‘transferable ruble’ tied to the resources of Russia (oil and gas, metals, gold, grain). At the same time, we must oblige importing countries to supply goods for rubles (transferable rubles) according to the rules required by us.”

To counter “the position of the United States and the IMF, it is advisable to agree on the recognition of the need to create national systems of protection against global risks of financial destabilization, including: the establishment of a system for regulating foreign exchange transactions of capital movements; a tax on income from the sale of assets by non-residents, the rate of which should depend on the period of ownership of the asset; providing countries with the possibility of imposing restrictions on cross-border movement of capital on transactions that pose a threat.”

Also, “it is necessary to accelerate the creation of a universal payment system for the BRICS countries and the issuance of a common BRICS payment card, combining Chinese UnionPay, Brazilian ELO, Indian RuPay, as well as Russian payment systems, as well as the transition to using their own rating agencies.”

“Once again, the Bank of Russia is driving our economy into a vicious cycle of decline: an increase in the interest rate – a squeeze on credit – a decrease in investment – a drop in technical level – a decrease in competitiveness – the devaluation of the ruble – rising prices.”

Glazyev has also calculated the damage to the Russian and Ukrainian economies – and what the economic benefit will be at the completion of the military operation. “The ‘Ukrainian factor’ and the external shocks caused by it have cost Russia, according to the most conservative estimates, up to $200 billion, and taking into account international sanctions, up to $ 0.5 trillion. Ukraine’s losses from the breakdown of cooperation with Russia and non-equivalent foreign economic exchange within the framework of the so-called association with the EU also amount to hundreds of billions of dollars.”

“In total, the improvement of trade conditions for Ukraine, according to estimates carried out on the eve of the coup in Kiev in 2014, would amount to about $10 billion, which would allow it to balance the trade balance and ensure macroeconomic stability. It should be borne in mind that other positive effects could be obtained by expanding trade in goods and services, intensifying scientific and technical cooperation, increasing investment and innovation activity in capital-intensive industries. Taking into account the cooperative spike possible with the EEC states in the future, the current and prospective macroeconomic effects for Ukraine could be much greater.”

“I believe that with the completion of the special military operation on demilitarization and denazification, it will be possible to open a new page in trade and economic relations with Ukraine, primarily with enterprises in the Lugansk and Donetsk People’s Republics.”

Glazyev is careful not to use the term “oligarch”, nor mention any of these well-known Russians by name. He has been targeted by them, and by their government representatives, Chubais and Kudrin, in 1996 when he was a leading figure in Alexander Lebed’s election campaign against Boris Yeltsin; in 2004 when Glazyev himself ran against Putin in the presidential election of that year; and when he was forced out of his Kremlin economics post in 2019. By implication, though, it’s clear from his list of priority industries for special CBR financing, capital export controls, and nationalization of exiting foreign companies that Glazyev’s plan for the war economy allows no place for the diversion of capital which has characterized the oligarch economy until now.

Delyagin is more outspoken against the oligarchs. In April, he cited public speeches by Yevgeny Savchenko (right) the former Belgorod governor and currently a senator representing the western region in the Federation Council; Savchenko is a member of the United Russia ruling party and a supporter of Putin.

According to Delyagin and Savchenko, the war economy requires “a basically new form of public ownership of the means of production, the principles of which are an economy without oligarchs; justice instead of exploitation; prosperity instead of poverty; development instead of stagnation. This can be done if the employees of enterprises become co-workers, that is, they will receive a part of the enterprise, plus profit in dividends. The share of the authorized capital that can become the property of the employees of the labour collective should be determined – preferably at least 30% and not more than 70%.”

This is what Glazyev has called the “labour collective” approach.

“Such a model,” Delyagin proposes, “does not necessarily represent the economy of [Soviet] socialism; there is even no restriction on the rights of an entrepreneur — the owner can retain a large stake and enjoy great influence.” However, Delyagin concedes there is powerful opposition. “The Russian leadership which has reappointed Ms. Nabiullina to the post of chairman of the Bank of Russia shows it is unlikely that the elite are looking for any change in the status quo. People follow the principle that you don’t change horses in midstream. [Senator] Savchenko’s ideas are quite reasonable, but such ideas have been ignored for 35 years and will continue to be ignored, in my opinion.”

In remarks last month as chairman of the Duma Committee on Economic Policy, Delyagin directly attacked steelmaker Vladimir Lisin and the two oligarchs with control stakes in the auto industry, Alexei Mordashov (lead mage, left) and Oleg Deripaska (right), for their attempts so far to take the lion’s share of the new state financial assistance: “The oligarchs should be deprived of the opportunity to have any relation to the new programs. The most significant is NLMK’s [Lisin’s Novolipetsk Metallurgical Combine] recent statement about the need to develop import substitution for steel parts. Obviously, the structure of billionaire Vladimir Lisin was just asking for money! It will be the same with UAZ (owned by Alexei Mordashov’s structures) or GAZ (owned by Oleg Deripaska). The money of the above-mentioned characters isn’t chicken feed. But to invest at least a penny of it in Russia, the oligarchs don’t want. On the other hand, grabbing government financing is always welcome!”

The new regulations and the bureaucracy to administer them are only a few weeks old; many of the legislative instruments and ministerial rules remain unfinished; under the requirement for wartime secrecy, lobbying, discretionary decision-making, and uncertainty are pervasive. From the Moscow business press this inventory of recent announcements has been compiled to show that for the time being the direction of asset redistribution appears to be in the oligarchs’ favour; and also that exiting foreign companies are concealing terms for buyback from Russian nominees when — they are calculating — the pressure from US sanctions and Ukrainian propaganda will lessen.

- Vladimir Potanin’s holding Interros has expanded his Rosbank business with a discount-priced, Central Bank-backed acquisition of the control stakes of Rosbank from the exiting French Société Generale and of the TCS (Tinkoff Credit Services) banking group from Oleg Tinkov. Private Eye, a London publication which has been following MI6 in its Russia reporting, endorses Tinkov’s allegation that he was forced into selling at a fraction of his asking price, and then complains that “Tinkov is on the UK sanctions list. Potanin is not;” Private Eye concealed Tinkoff’s conviction on US tax fraud charges late last year. Potanin has also made an offer for the departing Italian bank Unicredit’s assets; Unicredit and Citibank are negotiating the exit price for their assets with other Russian banks not under US sanctions.

- Vadim Moshkovich’s Rusagro group has taken over the assets of the exiting Finnish food product manufacturer Valio. Like Potanin, Moshkovich is not under US sanctions.

Left, Putin with Potanin, Moscow 2020; right, Moshkovich with Putin, Vladivostok September 2018. For more on Moshkovich, click.

- Highland Gold, formerly owned by Roman Abramovich and Viktor Vekselberg who sold to Vladislav Sviblov of the PIK real estate group, is buying out the eastern Russian goldmines of the Canadian miner Kinross Gold. Sviblov is not under sanctions; VTB which is financing the deal is sanctioned.

- Anglo-Dutch Shell will sell its large chain of petrol retailers in Russia to domestic rival LUKoil. LUKoil is sanctioned, but not Alekperov.

LUKoil’s controlling oligarch Vagit Alekperov with the President.

- The Spanish oil and gas company Repsol has sold its field exploration assets to the state-owned Gazprom Neft. Gazprom Neft has also bought out Shell’s half-share in the Arctic region explorer and developer, Gydan Energy.

- AvtoVAZ, the leading Russian car builder controlled by Renault, has been returned to a Russian state holding for a nominal rouble. However, the existing French firm has a buyback option which it may exercise within the next six years. For Delyagin’s attack on the failure of Renault and other foreign auto companies to encourage import substitution, read this.

- Polish clothing producer and retailer LPP SA, which has traded in Russia under the brand-names Reserved, Cropp, House, Mohito, and Sinsay, has announced it “is already negotiating with potential buyers”. Rival European clothing retailers H&M (Sweden) and the Inditex Group (Spain – brand-names Zara, Massimo Dutti, Pull&Bear) have also closed their stores but reported no sale talks. LPP’s Warsaw listed share price, which started falling sharply in February, has begun to recover on the expectation of a Russian takeover.

EXITING EUROPEAN COMPANIES RECOVER SHARE PRICE

KEY: grey=Kinross (Toronto); yellow=Société Generale (Paris); green=LPP (Warsaw). Source: https://markets.ft.com/

- The Russian tobacco and cigarette market, the fourth largest in the world, is being redivided as internationals Philip Morris, British American, Japan Tobacco and Imperial Brands make public announcements of their exit, combined with schemes to transfer assets to local partners, either by outright sale or with buyback and nominee schemes for returning. Igor Kesaev, the Russian cigarette oligarch, is a prime beneficiary. Kesaev is not sanctioned.

- In the bakery products market, Fazer, one of the largest food producers in Finland, announced it was selling its Russian subsidiary on April 29; this unit operated four bakeries whose annual revenues amounted to the Fazer group’s third largest country result after Finland and Sweden. The revenue reported in Russia in 2021 came to €157.4 million. The sale price to the Kolomensky Baker & Confectionery holding of Moscow remains secret but has been estimated at about $50 million.

- Soft drinks. PepsiCo, which bought out Wimm Bill Dann, a soft drinks producer, in 2010, announced the suspension of its Russian beverage businesses in March, and subsequently agreed to sell the drinks division of Wimm Bill Dann to Multipro, a small local cheesemaker. Since no transaction price or deal terms have been disclosed, and Multipro lacks the asset base itself for a market-value takeover, it is suspected either that PepsiCo is retaining a buyback option but keeping it secret; or that a major Russian group like Miratorg is planning a move into the beverage market and is still negotiating terms with the government.

- The Finnish coffee supplier Paulig, one of the largest in the Russian market, has sold its Tver roasting plant and distribution business to an Indian manager who has spent most of his career working for the Kesaev group’s grocery division. The Paulig deal may be a full buyout by Kesaev at a bargain price, or it may be a deferred buyback operation by the Finns.

- Alexander Govor buys out McDonald’s fast-food restaurants. Govor’s initial wealth came from privatizing coalmines in Novokuznetsk region and selling them to Evraz, the steelmaking group of Roman Abramovich and Alexander Abramov. Govor subsequently became a leading franchisee of the McDonald’s chain with 25 restaurants. In the new deal he will reportedly buy out more than 715 US-owned restaurants in the chain, and replace their brand name. No transaction price has been revealed; the asset value writeoff by the parent company from the closure has been reported in the Russian media to be $1.4 billion. The outcome for the potato farms and processing plants also owned by McDonalds for supplying the restaurant chain, is unclear.

Left to right: Igor Kesaev; Alexander Govor; the President, Victor Vekselberg.

- The Swiss pump and engineering company Sulzer announced on May 24 that it will withdraw from Russia, and sell its businesses there. The company which until 2018 was controlled by Victor Vekselberg with 63% of the shares, bought back enough of his shares after he had been sanctioned by the US, reducing his stake to 48%. It is not known if Vekselberg will buy the Russian assets using funds which Swiss officials have frozen under US pressure.

Remaining in office as a powerful advocate for the oligarchs, Alexei Kudrin appeared on May 25 before the State Duma to provide his annual report on the work of the Accounting Chamber, the state audit agency which he has directed since 2018.

Source: http://duma.gov.ru/news/54396/

Before this, Kudrin had been in Israel for several weeks of medical treatment for what is believed to be prolapse of the spine. While undergoing treatment in Tel Aviv, Kudrin met his career patron Anatoly Chubais, who has exiled himself from Russia. In his public speeches Kudrin has avoided criticism of the military operation. Instead, he is forecasting the worst losses in the economy since the end of the Soviet Union.

Leave a Reply