By John Helmer, Moscow

It’s no surprise that when Alisher Usmanov (left) proposed an initial public offering (IPO) of Megafon, a mobile telephone company he controls, he decided to keep all his shares to himself, and to oblige new sharebuyers to bid for stock being sold from the treasury of Megafon, and from minority stockholder, Sweden’s TeliaSonera. That makes the IPO less a wager on the profitability of Russian telephones, more a referendum on who wants to be Usmanov’s minority shareholding partner.

It is also unsurprising that Goldman Sachs, one of the two co-managers engaged in June to manage the IPO, refused to do so, resigning days ago, just before Megafon completed its prospectus. Goldman Sachs didn’t have such a problem being co-manager of the listing of Yandex, the Russian search engine company, in April of 2011. In December of 2011, Goldman Sachs didn’t walk away from its role as co-manager in a $500 million loan syndicate for Vimpelcom, one of Megafon’s domestic competitors.

Finally, it is not surprising that Usmanov and the Megafon management want to cover up this powerful vote of no-confidence before the IPO hits the roadshow stage by delaying the release of the IPO prospectus; and by refusing to go into the reasons for the disappearance of Goldman Sachs from the underwriter list. In June, Bloomberg reported Goldman Sachs had been hired, along with Morgan Stanley, Sberbank, VTB Group, Credit Suisse, and Citigroup. The list today is the same, minus Goldman Sachs.

The Megafon company announcements to date advertise the London stock sale as an investment in Russian GDP growth and the concomitant profitability of the growing telephony business – mobile, advanced fixed-line, data transmission. “The Company,” according to an October 9 release, “is Russia’s 2nd largest mobile operator with c.62m subscribers representing a market share of over 27% as of the six months ended 30 June 2012, (according to AC&M) and the largest operator in the mobile data segment since 2008, a market which has grown at a CAGR of over 44% from 2009 to 2011 (according to Informa Telecoms and Media).”

“The Russian mobile data market is forecast to grow at a CAGR [compound annual growth rate] of 21% from 2011-2015 (according to AC&M) with potential for low existing smartphone and 3G penetration to catch up with Western European levels. The Company believes it is well positioned to exploit the potential further growth of the Russian mobile data market as it operates the most extensive 3G network in Russia, offering high performance and service quality. It was the first of the Big Three [Megafon, Vimpelcom, MTS] to offer LTE/4G high-speed mobile broadband data services to its clients and expects to be in a position to offer its LTE/4G services in over 40 cities, including Moscow and St Petersburg, by the end of 2012. Similar room for growth exists in value added services, where the Company aims to develop innovative services and content.”

A detailed report on Megafon, dated September 12, by the head of research at Uralsib Bank, Konstantin Chernyshev, provides a handy reckoner of the valuations already applied to Megafon in private stock sale transactions this year; and of IPO valuations using standard financial methodology. Chernyshev indicates a valuation spread between $13 billion and $19 billion. VTB, one of the official underwriters, has allowed it to be known that its value range for Megafon’s market capitalization is from $12.6 billion to $15.1 billion.

At the Uralsib Bank valuation of $13 billion, or $24 per share, Megafon’s price to earnings ratio would be 10.5; that’s below the already listed shares of Vimpelcom (Mikhail Fridman’s property) and MTS (Vladimir Yevtushenkov of Sistema). It’s 25% below the median ratio for mobile telephone companies in the emerging markets outside Russia. Only Magyar Telecom and China Mobile come close, the Hungarian slightly worse, the Chinese slightly better.

Compared to the developed market mobile operators, where growth rates and profitability are much poorer, on Chernyshev’s calculations Megafon would be priced at an 11% premium on this year’s numbers, but at a 5% discount next year.

The company’s IPO announcement fudges on who is actually selling the shares. “The IPO is expected to comprise a proportion of the existing ordinary shares in MegaFon held by Sonera Holding B.V., a subsidiary of TeliaSonera A.B. and by MegaFon Investments (Cyprus) Limited (“MICL”), a subsidiary of MegaFon.” This begs the questions of why the Swedes are selling down their stake and by how much. Asked what the shareholding line-up will be if (after) the IPO goes ahead next month, Megafon’s Moscow and London spokesmen believe it’s too early to say.

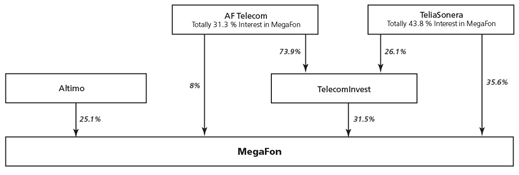

Chernyshev’s report provides two charts for a clearer picture. Here is the shareholding structure at the start of this year, before Fridman sold Usmanov the Altimo stake of 25.1%:

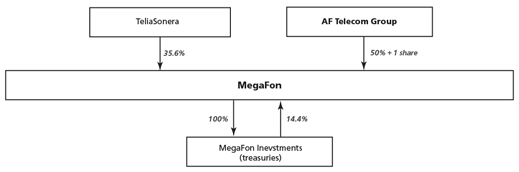

And here is the pre-IPO structure, with Usmanov inside the AF Telecom box with 50% plus one share:

The Financial Times and the Moscow business press report today that the effect of the share sale will be a dilution and redistribution of minority shareholders, and a concomitant strengthening of Usmanov’s position in control of the company. According to these reports, TeliaSonera will go down to 25%, and part of the Megafon Investments’ (treasury owned) 14.4% will be sold. The demand in the London market for these shares will dictate how few of them should be sold in order to sustain a sale price that doesn’t oblige Usmanov to accept a heftier discount than he thinks he’s worth – a financial vote of no confidence. It was reported earlier that a 20% bloc of shares would be sold – 10.5% from TeliaSonera, 9.4% from Megafon Investments. But if the sale volume is cut to 15%, it isn’t known if TeliaSonera will insist on getting rid of the planned 10.5%.

There is also a fudge in Megafon’s IPO announcement on what is to be done with the share sale proceeds: “The offering and listing is [sic] intended to enhance the Company’s capital markets profile and access, providing strategic flexibility to support its long term growth and development. The Company intends to use the net proceeds of the offering (received from the sale of shares and GDRs by its subsidiary MICL) to repay and/or finance existing debt and for general corporate purposes including the continuing development and expansion of its network.”

According to Cherynshev at Uralsib Bank, “as of June 2012, MegaFon had RUB156 mln ($4.8 bln) of net debt, which is rather low, equivalent to a 2012E EBITDA of 1.4. The debt load should decline after the IPO, as half the proceeds are reportedly being planned to go back into the company.” That depends on the Swedes. If they intend to carry off all of the cash generated by the sale of their shares, and if the volume of the treasury shares which can be marketed drops, the proceeds returned to the company will dwindle. The debt will be reduced by significantly less. Megafon isn’t saying what will happen, partly because it isn’t sure yet how the London market will view the offering.

And this is what makes Goldman Sachs’ s exit so telling. Goldman Sachs has done this before. In 2006, for example, after the investment banking division of Goldman Sachs promoted participation in the IPO of Dmitry Pumpyansky’s steel pipemaker, TMK, the bank’s risk committee took fright. Among the concerns that Goldman Sachs officials debated among themselves at the time was the history of the TMK asset consolidation by Pumpyansky and a group of robust fellows known as the Uralmash gang. Credit Suisse didn’t have the same qualms, and remained in the TMK share sale then. They are sticking with Usmanov this time round.

The problem for Usmanov is a combination of what has been documented in US and Swedish courts about his methods and behaviour towards shareholding partners in the past; and of what is believed about the methods of his Russian partner, Andrei Skoch, in the consolidation of their assets. Usmanov and Skoch have tried testing the London market many times, and the reaction has been consistently negative. The failure to list and sell shares of Metalloinvest — Usmanov’s and Skoch’s steelmaking and iron-ore mining company — has been repeated several times over. This time round, although the UK regulators have allowed the IPO to proceed, Usmanov let slip a compromising detail during a promotional tour he recently gave Reuters of his mind.

His plan, he told two reporters over “tea and central Asian delicacies at his mansion outside Moscow”, is to create an umbrella holding of his assets, including Megafon. The umbrella, he said, “will be owned with his partners Farhad Moshiri, with whom Usmanov owns a stake in London soccer club Arsenal, and Vladimir Skoch, father of billionaire lawmaker Andrei Skoch, who helped build up Metalloinvest, the world’s fifth largest iron ore company.” Moshiri has been Usmanov’s dogsbody for years. But why should Andrei Skoch, a member of the State Duma, who doesn’t talk about his business, pass his torch to his father, reportedly at least 80 years of age? This was an oriental delicacy the Reuters reporters lacked the taste to appreciate. According to what Usmanov told them, “we are not against being public – but not because we want only to be public, but because I think it is good for our partners. If we see the level of the valuation as good, we go to IPO.”

For Goldman Sachs, this was tantamount to inviting the London market to put a value on Moshiri, Andrei and Vladimir Skoch, with the added implication that Usmanov may be intending to divide the control stake in Megafon with Moshiri and the Skoch family; maybe to have Vladimir Skoch supervise Megafon. That’s in the event Usmanov finds something else to do. “Honestly,” Reuters reported Usmanov’s self-effacement, “I don’t want to do business any more, but you have a responsibility towards business that you (already) have.”

Usmanov’s success in lifting the share price of Mail.ru, the social network and game portal company which he listed in November 2010, has been equivocal.

SHARE PRICE TRAJECTORY FOR MAIL.RU SINCE LONDON LISTING, NOVEMBER 2010:

Ivan Tavrin, a 36-year old local ad man, was put in charge of Megafon six months ago after a stretch in one of Usmanov’s television ventures. He is reported by the Financial Times as explaining the reason for Goldman Sachs’s exit to have been timing. “This is [a] process where all the horses need to run on one time and it’s quite a challenging job for a company to manage six banks in one process. Everybody should be on the same page in terms of timing.” His London spokesman confirmed today Tavrin had said that. The Moscow spokesman said the correct quotation of what Tavrin had said appeared in Kommersant. “Yesterday, we announced plans to hold a public offering of MegaFon by the end of the year, and we are working with the banks, which were ready to organize the IPO in these terms. In this process, a complete and very precise coordination of the process and the work of all parties should be fully secured in uniform terms. As part of the five largest banks in the syndicate, the two Russian and three international, we are completely satisfied. As for Goldman Sachs, we work with them, and many other banks on different projects.”

Leave a Reply