By John Helmer, Moscow

@bears_with

Belgium has decided to host its second Battle of Waterloo in two hundred and eight years, this time on Napoleon’s side. But on this occasion it won’t be, as the Duke of Wellington claimed before, a “close run thing”.

In the last episode of the Napoleon-sized mistakes the US and NATO are making in their sanctions war against Russia, the battleground was at sea. There, the sanctions war has transformed the global movement of oil and gas tankers – the routes, ports, insurance, contracts, pricing, certification, and recording. The major commercial and state fleets have now split into two blocs, ending the unified global tanker market and returning to the conditions of secrecy, smuggling, and bypass port hubs last seen in Europe when Napoleon attempted to impose his blockade of British merchantmen in what was called the “Continental System” at the time. That was more than two hundred years ago, between 1806 and 1814.

France did not recover from the damage the over-confident Napoleon did to the French position in Europe’s seaborne trade. Napoleon multiplied the cost of his misjudgement by deciding that, in order to enforce his blockade, he should invade Spain, Portugal and Russia, and close their ports. Russia then buried Napoleon twice — once in Moscow in 1812, then in Paris in 1814, before he and the French army were finished off at Waterloo. This time round, the US-NATO blockade of the Russian tanker trade is Napoleonic in the obviousness of the miscalculation; it is also Napoleonic in the magnitude of losses on the NATO side — and the acceleration of profits on the Russian side.

In today’s new episode, the battleground is the diamond trade based in Antwerp, Belgium.

Almost $14 billion worth of diamonds are imported annually for cutting, polishing, and trading there, and about the same value is exported. In their rough form, most of the diamonds in the Belgian market have been mined in Russia, and either sent direct to the Antwerp diamond market, or indirectly through India. Most of the diamonds exported from Antwerp have been going to India, United Arab Emirates (UAE), and Israel. The Israeli diamond processing business exports mostly to the US jewellery market.

The diamond trade in Europe has traditionally been a Jewish operation; until the Germans arrived in 1940 that was based in Amsterdam, Netherlands, for four hundred years. German race hatred wiped out the Jews of Amsterdam; Belgian race hatred for Russians is about to wipe out the Antwerp diamond market. The Jewish business is about to become an Arab one. As one Antwerp diamantaire described the situation, “if the Belgian government thinks it’s giving the finger to the Russians, all that will happen is that the diamond on that finger will move, and the finger will be what Dubai will be pointing.”

Martin Rapaport’s price sheet for the trade in Tel Aviv and New York reports that in Belgium “sentiment [is] very low. Serious concerns for coming months. 0.50 and 1 ct. [carat] diamonds especially weak due to sluggish US orders. Many hope holiday activity will kickstart trading. Uncertainty surrounds Russian diamonds as fresh sanctions loom.”

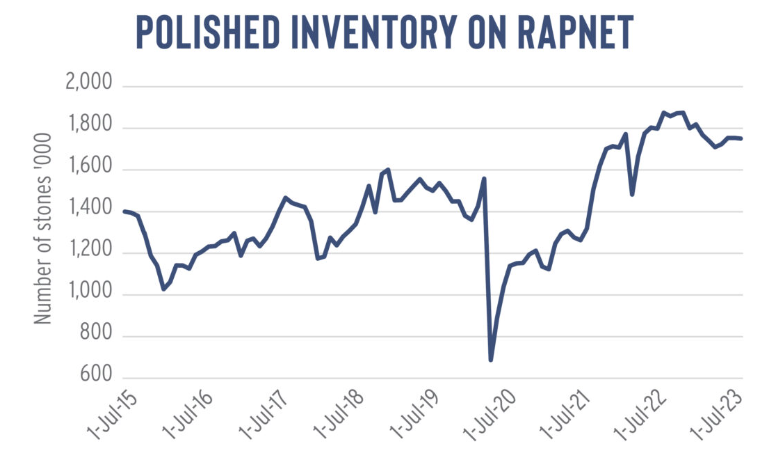

Rapaport, a dual Israeli-American citizen and self-reported “world’s largest and most trusted marketplace for diamonds & jewelry”, has been promoting fresh sanctions against Russian diamonds to cut the volume of Russian rough in the global market; these have been causing diamond inventories to overflow, diamond prices to fall, and Israeli margins to shrink. “Russia was the wild card in 2022. Whereas it was assumed the sanctions imposed in February by the US on Russian-sourced diamonds would lead to shortages, the goods continued to enter the market — propping up polished inventories.”

Rapaport’s fix is heavier US artillery in the war against Russian diamonds.

“There is a need,” he editorialised on July 12, “to address the issue of ‘substantial transformation’ — a pathway through which the current US sanctions still allow Russian-origin rough diamonds to enter the US if they are cut and polished in a third country, as explained by the Jewelers Vigilance Committee (JVC). The Group of Seven (G7) nations — Canada, France, Germany, Italy, Japan, the UK and the US — are working on measures that will require companies to disclose the origin of their diamond imports, both rough and polished.”

Rapaport was endorsing the attack on the Belgians by Vladimir Zelensky of the Ukraine, speaking to the Belgian parliament: “There are people”, he said, “for whom the diamonds sold in Antwerp are more important than the battle we are waging.”

Following Rapaport at the end of August, Brad Brooks-Rubin of the US State Department’s Office of Sanctions Coordination and career Russia diamond-fighter, announced that consumption of Russian diamonds must be stopped in the G7 nations, which currently account for almost 70% of all diamond purchases. “By cutting off most of their demand, if an import ban were to be agreed, Russian diamonds would have a narrower lane through which to work their way into the marketplace,” he said. “The focus of all discussions is how to target Alrosa and Russia’s diamond revenues that could then be funneled to their war efforts.” Like Rapaport, Brooks-Rubin is also a dual national.

In New York three weeks later, Belgium’s prime minister Alexander De Croo followed with an announcement of his new sanctions plan against Russian diamonds: “Russian diamonds are blood diamonds,” he said. Beginning January 1, 2024, “the G7 has a goal of banning Russian diamonds from the market. [We still must go] the final mile. We are extremely happy to play a role in this [effort]. We are a partner in this.” The new sanction, he said, is “good and strong and makes sure that we don’t have to have second thoughts about what is being sold.”

The plan is that anyone importing rough or polished diamonds into a G7 country, including the US, would be required to declare on their invoices that their shipments do not contain Russian diamonds, either original rough from Russia or processed in a third country. The plan puts Russian rough on a par with the so-called “conflict” or “blood” diamonds from Africa and Kimberley Process, which have been under source and invoice tracking for twenty years.

De Croo is no Napoleon. He is losing control of a weak coalition of minority government parties; his own party, the Open VLD (Flemish Liberals and Democrats), has dwindled in the polls to single digits since the beginning of the year; he faces oblivion when the Belgian election is called next June. The diamantaires of Antwerp are viewed in this election as carpetbaggers, not Belgians.

Portraying the new anti-Russian diamond move as a “European Union” initiative won’t save the plan or De Croo, Belgian sources comment. They believe the global diamond market will be split into two blocs, and what will remain for Antwerp will be the diminishing, high-cost market of Europeans and Americans. When they are defeated on the Ukrainian battlefield, the sources expect Antwerp will not recover, and Dubai will boom.

“I cannot see [the new sanction plan] working, especially for polished,” adds a leading London diamantaire. “How will polished be traced as Russian? Despite the so-called technology it won’t happen, as people will dream up ways around.”

The first US sanction hit the import of Russian jewellery diamonds at the same time as Russian caviar and vodka. That was on March 11, 2022.

Left: https://www.whitehouse.gov/

The US sanction against Alrosa, the state diamond mining leader, followed in April 2022. Right: Martin Rapaport.

Rapaport’s publication has acknowledged the failure of the US move, but claims not to know how the work-around diamond trade is operating. “Russian diamonds are entering India, Belgium and other global trading centers. Everyone acknowledges that. But it’s unclear how the goods are getting there, what the volumes are, and which banks are handling the payments. One rumour on the market is that Russian miner Alrosa, a sanctioned entity in the US, has set up a subsidiary that sells rough to manufacturers, perhaps via an intermediary. Some say Alrosa goods have been reaching Mumbai and Surat via Dubai, though this pathway seems to have ceased due to banking problems. By almost all reports, the flow of Russian rough into India has declined since the start of the Ukraine war in February 2022. Shipments slowed in last year’s fourth quarter, though few people who spoke with Rapaport this past February were able to explain why. It appears certain banks became less willing to approve money transfers to Russia, either voluntarily or under the influence of governments.”

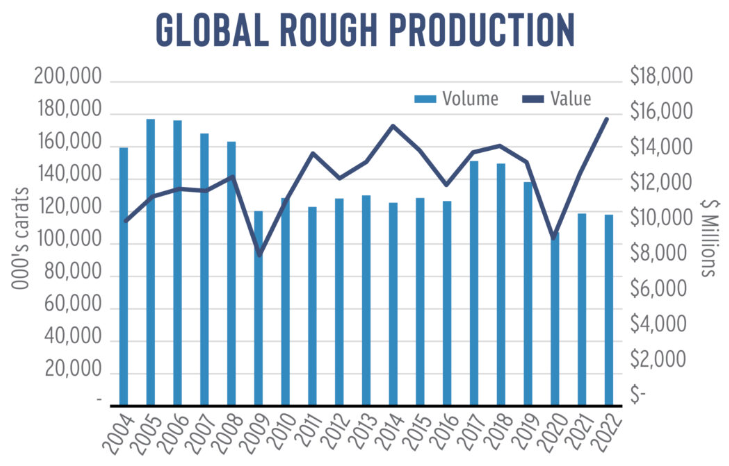

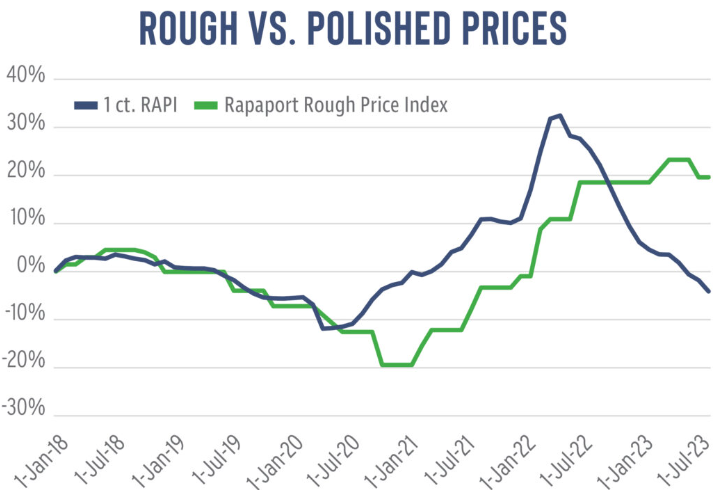

“The Russia crisis is forcing the diamond trade to take responsible sourcing to the next level”, Rapaport declared.

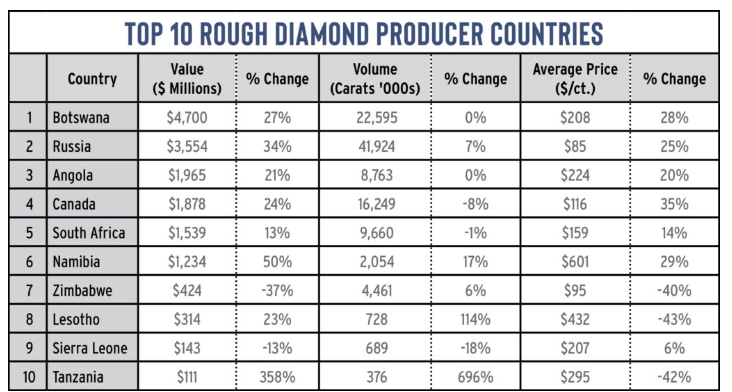

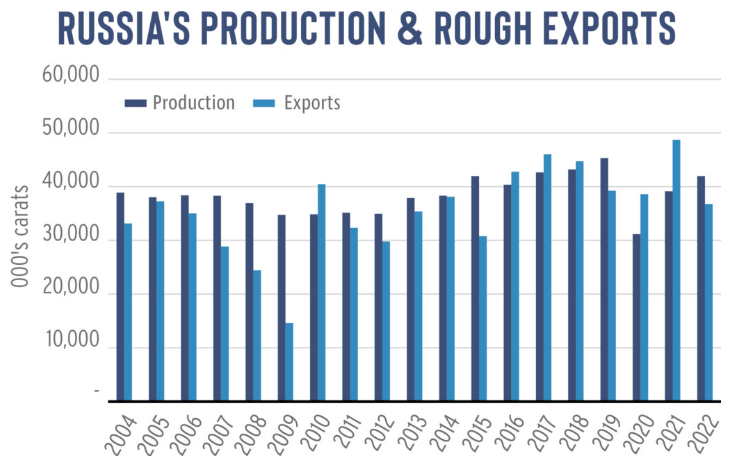

In five charts Rapaport and his analysts have demonstrated that between 2021 and 2022 Russian rough diamond production and exports have been growing modestly in volume (7%) and sharply in value (34%). At the same time, global rough prices have continued upward, but polished prices have been falling. As a result, unsold inventories of polished have been accumulating, hurting the pockets of the Tel Aviv-New York trade.

These charts also illustrate how the US sanction of March 2022 has turned out to be much better for Alrosa, the dominant state-owned diamond mining company, than the warfighters expected, or rivals like De Beers of South Africa and Botswana were hoping. Like Napoleon, De Croo can read charts; like Napoleon, his political survival in Brussels depends on his fighting the short-term battle because the long-term war is beyond his next election.

Source, all charts: https://rapaport.com/

For the last round of the diamond sanctions, Alrosa’s resistance, and De Croo’s ambivalence, read this.

For thirty years this reporter has led English-language coverage of the Russian diamond business; the website archive on Alrosa can be followed here. When reader demand for military news declines and for Russian business returns, there will be a book on how the diamond wars were fought between Alrosa and De Beers, how the Russian oligarchs fought over the diamond mine in Arkhangelsk called Grib — and who won.

For an assessment of De Croo’s speech in New York last week, and the prospects for the new sanction as gauged by the US diamond business, click to read.

The implication in this report is that behind closed doors in Antwerp, the Belgians, Israelis, and Indians will connive at working around the new tracking system.

“The Belgian government’s plan, which is backed by the Antwerp World Diamond Centre (AWDC), requires traders to verify their declarations with information from existing tech-based traceability programs, including Tracr, the GIA’s Diamond Origin Report, Sarine Diamond Journey, Everledger, and others. All the tech information would be synthesised into a blockchain-supported ‘public ledger’ for which the GIA [Gemmological Institute of America] would provide technical support. Proponents argue this moves the burden of proof ‘upstream’ toward miners and cutters, and would allow the trade to make far-reaching changes that could extend beyond the current issues with Russian diamonds. ‘This will make traceability standard in the industry,’ says an Antwerp source, arguing that the trade won’t change unless it’s forced to. ‘If you’re not told to sort your trash, then you won’t sort your trash.’ The Belgian proposal says that all rough must be tracked and traced by one of these systems and pass through a ‘rough node.’”

“In a departure from trade custom, it says that ‘only unmixed [i.e., single-origin] parcels of rough diamonds directly from the source’ would be allowed into G7 countries, though it makes an exception for goods from De Beers’ Botswana sort. (‘Beneficiated goods,’ meaning diamonds polished inside the country where they were mined, would not have to pass through this rough node.) Once cut, the diamonds would pass through a ‘polished node,’ located in a G7 country, which would determine if the shipper has the required backup. On a practical level, this would likely reroute goods to Antwerp for ‘prescreening,’ as Antwerp has a fully staffed Diamond Office, while most other countries don’t. That has led some to dub the Belgian proposal self-serving, noting that until recently, Antwerp officials vocally opposed sanctions on Russian goods.”

“The Antwerp source acknowledges that the centre would benefit in the short term, but argues the city would probably not serve as the sole node indefinitely.”

No source in the diamond business will talk about this on the record; no Russian source has been contacted for comment.

According to a European source, the work-around diamond plan focuses on direct diamond shipments from Moscow to the Indian diamond-cutting centre in Mumbai and to Dubai. “If/when European sanctions do take place, Dubai and India direct would naturally benefit further. There will however always be a small amount of polishing, sorting and other added value methods in Antwerp, whereas there is none to speak of in Dubai – it is still mainly a geographically convenient and tax advantageous postbox for rough, some of it of dubious African origin. You do still see crowds of Indians, and some Israelis, in the Antwerp diamond quarter streets and offices during the appropriate periods of each five-week ‘sight’ cycle.”

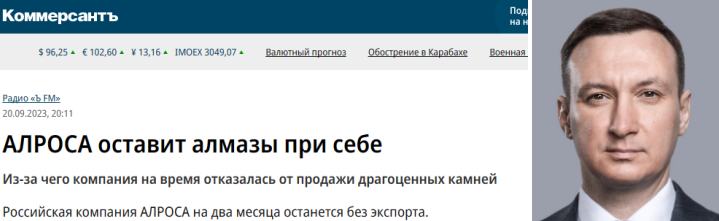

Last week the Moscow business daily, Kommersant, published a report on the new agreement between Alrosa and the Indian industry to reduce the flow of rough in order to sustain market price stability.

Left: Kommersant report of last week. Right: Alrosa’s new chief executive, Pavel Marinychev, appointed in April of this year; he succeeded Sergei Ivanov, who was personally sanctioned by the US in February 2022, both for his role at Alrosa and also because he is the son of Sergei Ivanov, “one of Putin’s closest allies”.

“The Russian company Alrosa will remain without exports for two months,” Kommersant reported. “The diamond producer made this decision at the request of the Indian authorities, who indicated that the demand for precious stones is already declining. In addition, the so-called Diwali season begins soon in India – the largest religious holiday, because of which the country goes on vacation for several weeks. Alrosa, as it is said in the message, fears that diamonds will not be cut during this period, which will lead to overstocking of the market and, against the background of a decrease in demand, will bring down prices. As a result, the company refused to distribute raw materials in September and October.”

“We are talking about coordination of actions between producers and processors of diamonds in order to prevent overstocking of the market. This generally fits into the strategy of the Russian company to maintain prices for precious stones, which, let me remind you, are falling. So, since the beginning of the year, the price of diamonds has decreased by 15%… As for Alrosa’s revenues, the company is helped by a weaker ruble and the absence of a one-time mineral extraction tax in the second half of the year. Accordingly, there is an opportunity to keep the profit at least in ruble terms.”

“The G7 countries account for about 80-90 million carats of diamond consumption per year. As for India and China, this figure is at the level of 60 million carats. That is, the Group of Seven is ahead in this area, but taking into account the fact that Russia produces about 40 million carats annually, India and China can take all this volume. As for the possible restrictions in this industry, I think the situation will be similar to similar sanctions against oil, which is now being quietly sold to India and China, albeit at a certain discount to the world price. As far as I understand, after cutting, it is quite difficult to separate diamonds of Russian origin from other stones. But if, after all, technology will somehow control the process of selling diamonds, then the Russian Federation, taking into account the capacity of the markets, can really send supplies to developing countries. Russian production is less than demand in developing countries.”

A London diamantaire agrees the global diamond market will split, enhancing the importance of the alt-Antwerp trading centres, Dubai for India and Shanghai for China.

“I cannot see it working, especially for polished. Briefly, no Russian rough has passed through Antwerp or Dubai since about July 2022. It all goes directly to India, simply because Indian banks are prepared to finance the purchases in rupees or rubles. Belgian and UAE banks cannot because of transactions being in US dollars. Possibly some Grib diamonds went to Dubai last year, but not much. It is all about finance, not the diamonds themselves.”

“How will the polished be traced as Russian? Despite the so-called technology it won’t happen, as people will dream up ways around. As to Antwerp versus Dubai, it has been predicted for so long, yet Antwerp hangs on. Most of the big Jewish firms have a presence in Antwerp as do the giant Indian conglomerates. It is easy to exaggerate figures in the diamond business. There is plenty of room for both Antwerp and Dubai. I do not see it as one or the other.”

Leave a Reply