by John Helmer, Moscow

@bears_with

Russian toilet paper is a national secret – not a state secret, but a commercial one.

This is because production, sales and profits have been growing fast – and this has been for the past five years, before the current toilet paper panic.

Secrecy is also in operation because the major foreign companies would like to keep the lion’s share of the Russian market boom by out-selling or buying up the competing Russian toilet paper companies. They, in their turn, want to push the foreigners out by consolidating among themselves and lobbying for government measures to do that. Consolidation of assets and market share is what western market analysts call it. In Russia it can be called asset raiding. This is when one toilet paper company takes over a rival at a price for the assets which is below the real asset value.

In the bum boom, on the hot seat at the moment are Essity, a unit of SCA, the Swedish paper and pulp group group, which is currently the Russian market leader with a third of the market; Hayat Kimya, a Turkish group trying to expand from its base in Tatarstan; and Kimberly-Clark, the Kleenex maker of the US, which is losing market share to the Russian brands. SCA and Kimberly-Clark are stock exchange-listed shareholding companies with public reporting and accounting obligations. The Hayat holding is privately held. About their Russian business they are as secretive as each other. Altogether, the Russians produce just over half the toilet paper sold in the market; the Swedes, Turks and Americans, just under half. That proportion is about to change.

The five leading toilet paper brands in Russia are regularly surveyed and reported by Euromonitor International, the international market survey group. The most recent report, Tissue and Hygiene in Russia, was published in March 2019. Click to obtain a copy. The following table includes the most recent data for 2019.

THE TOP FIVE RUSSIAN TOILET BRANDS, THEIR OWNERS AND MARKET SHARES, 2015-2019

For enlarged image click to print Source: https://blog.euromonitor.com/

Two of these brands, Zewa and Linia Veiro (these are the names printed in English on the product package), are misnomers. Surprisingly, this appears to have been unanticipated by the producers; it goes unrecognized by the consumers. In Russian, Zewa comes from zev (зев in Cyrillic), which means a hole. Not the one for which the tissue is intended, but the hole through which food must pass between the mouth and the stomach – the pharynx. To Russians, Linia Veiro is half-meaningless; linia (линия) means a line, but veiro isn’t a Russian word. It’s Portugese, deriving from Latin. It means spotted or speckled; for horses, it means piebald.

Toilet paper is made mostly from cellulose, a byproduct of the conversion of timber to paper and pulp. More toilet paper sales require more cellulose supplies. Bigger toilet paper profit margin requires that the toilet paper producer owns his own source of cellulose, or is owned by a cellulose producer.

When it opened its new cellulose conversion and tissue manufacturing plant in Alabuga, Tatarstan, in December 2019, Hayat Kimya claimed that with an investment of $225 million, it had doubled its output capacity from 70,000 tonnes per year to 140,000 tonnes. It claimed to be “the largest cellulose cleaning paper producer in Russia”, with a market share of 17%. It also declared its goal to “become the largest paper producer in Russia”.

Hayat’s new plant in Tatarstan, with Turkish and Russian managers beside a delegation visiting from Ankara led by the Turkish Industry and Technology Minister, Mustafa Varank, December 2019. Source: https://www.dailysabah.

The Turkish market share is an exaggeration; the ambition to expand it depends, not only on the continuing growth of Russian consumer demand, but on the competition. The Russian rivals most likely to succeed are those who combine cellulose mills with paper production plants.

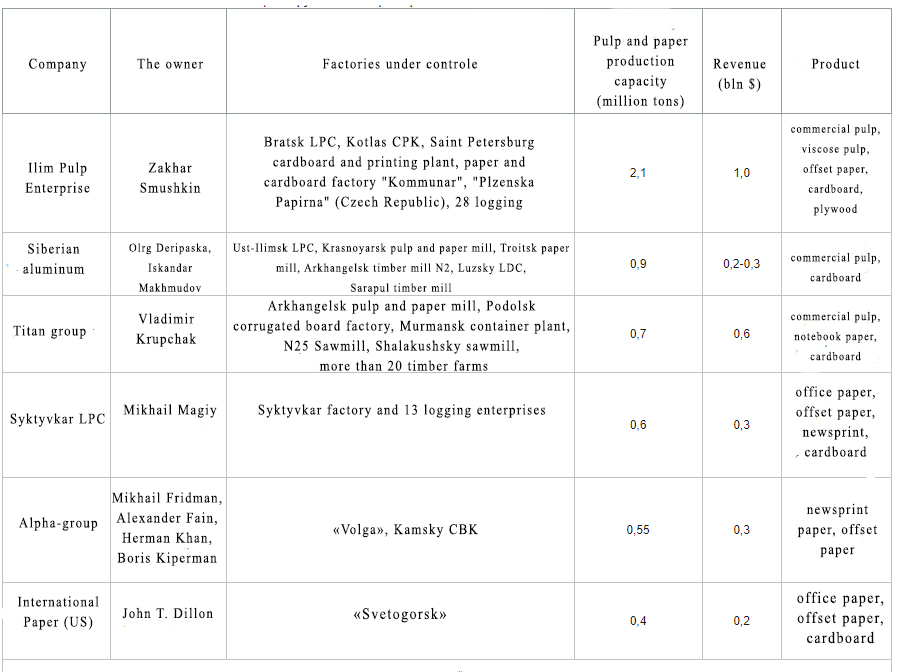

THE TOP FIVE CELLULOSE PRODUCERS IN RUSSIA, DECEMBER 2019

Source: https://expert.ru/

When it comes to competition for market share, three well-known oligarchs are best positioned to wipe the floor, at least upstream in the cellulose market. They are Zakhar Smushkin, Oleg Deripaska, and Mikhail Fridman. Smushkin defeated Deripaska for control of the Ilim Pulp group years ago, and for the time being neither of them, nor other oligarchs in the forest, timber, paper and pulp business, like Alexei Mordashov and Roman Abramovich, have tried to move downstream into toilet paper.

If the profit margin at that end remains high, if toilet paper prices rise, and if demand keeps growing, they will. Falling consumer incomes, less money to spend in the supermarket, and negative future prospects are a deterrent for the time being.

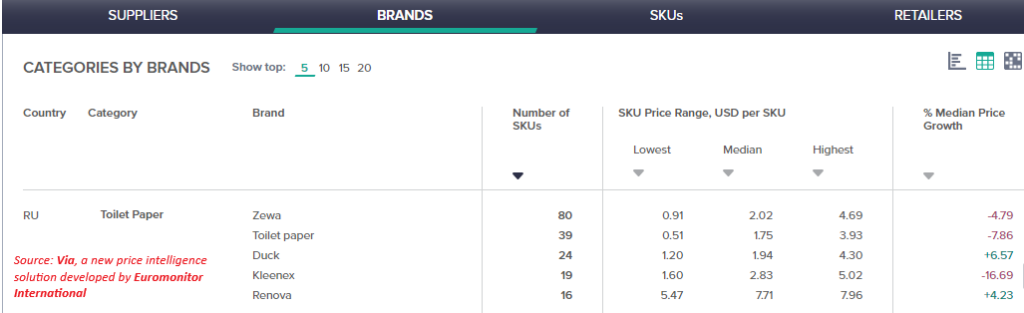

Euromonitor’s most recent survey of online toilet paper buying indicates that prices were falling between mid-February and this month.

PRICE DECLINES FOR ONLINE SALES OF THE TOP-5 TOILET PAPER BRANDS, FEBRUARY 16-MARCH 17, 2020

For enlarged image click to print

Key: SKU=stock-keeping unit marked by the product barcode. Source: Euromonitor VIA surveys: https://go.euromonitor.com/

Panic-buying and hoarding of toilet paper, which started in Australia and spread northwards, was slow to reach Russia, but it has now arrived, at least for the top-5 brands and most especially in the online retail segment of the market.

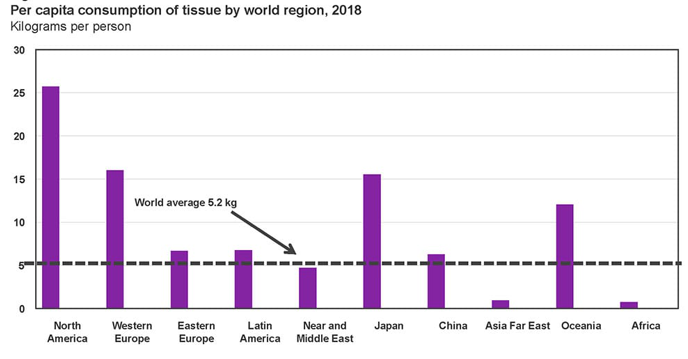

Until now, the acceleration in Russian toilet paper sales over the past five years reflects the relatively low consumer buying level of the past; the low quality of Soviet-era, single-ply paper which used to fill the market; and the improving incomes of most Russians. The Russian per capita consumption of toilet paper, plus paper towels, tissues and sanitary napkins, was 3.8 kilogrammes as of 2017. This was well below the global average.

Source: https://www.tissueworldmagazine.

For a measure of toilet paper consumption, read this.

The Russian average was also less than China’s and Mexico’s. The figure may be misleading; it is not to say that Russians wipe their bottoms less than the rest of the world. The Russian average includes a much higher share for toilet paper than in the other countries whose consumption numbers are boosted by the other paper categories. Toilet paper comprises 70% of the Russian number; in western Europe, 55%.

Russians are catching up. As a market analysis by Sergei Moiseev pointed out in mid-2018, “in recent years, Russia has experienced several economic crises, each of which has led to losses for businesses in a variety of industries. But only manufacturers of toilet paper feel equally confident in any situation: in Russia, this segment is growing by 6% a year under any conditions. A growing market, many major players, and no clear leader — this is the market for paper sanitary products in Russia.”

The market has also been transformed by the quality of the wipe. As Russian consumer income recovered from the 2008-2009 crisis, more money has meant less demand for the Soviet standard, one-ply toilet paper. By the end of 2016, the 2-ply product had reached 61% of total supplies; 3-ply had grown to 24%; one-ply dwindled to 12%; it had been about 60% in 2011. There was also a small but growing demand for a 4-ply product. Zewa called that its “Deluxe” model. Since 2016, however, the deluxe label on the package refers to 3-ply.

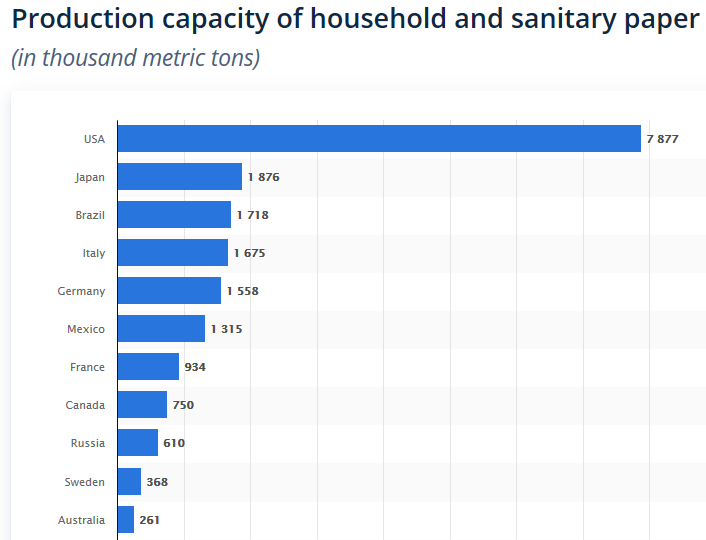

With enormous forest and timber volumes, Russia’s capacity to produce more cellulose and then toilet paper is considerable.

TOILET PAPER PRODUCTION CAPACITY, THE GLOBAL LEADERS – RUSSIA LAGS AT 10TH PLACE — 2017

With the addition of Hayat’s new volume last December and new plants in development, Russia should overtake Canada shortly and challenge France. Source: https://www.statista.com/

In terms of value of toilet paper sales, it’s numbers of bottoms which generate the biggest revenue number for China, with annual sales for 2019-2020 estimated at $16.6 billion. Cultural differences and toilet habits lift the US revenues to $13.3 billion, well ahead of India with $8 billion. Brazil comes next at $3.1 billion; Japan follows at $2.9 billion. The latest toilet paper sales figure for Russia can be calculated from the average per-roll sale price multiplied by the state statistics agency Rossat’s measure of annual roll production. For this year, the number will come to about Rb100 billion; at last year’s exchange rate value, that’s about $2 billion.

Who will profit?

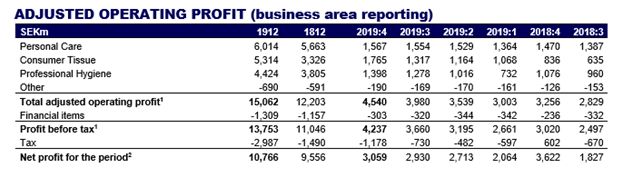

The three foreign producers – Essity (Sweden), Hayat (Turkey), Kimberly-Clark (US) – carefully avoid releasing details of their Russian business in their stock market reports or when asked directly. As a group operating worldwide, Essity-SCA is highly profitable. This report excerpt shows that the toilet paper and tissue segment of the group is showing a faster rate of profit growth, and is generating a larger proportion of the group’s bottom-line profit than the other product lines.

ESSITY-SCA ANNUAL REPORT, TOILET PAPER PROFITABILITY 2018-2019

Source: https://mb.cision.com/

However, Essity is stonily silent about its Russian toilet paper business, despite the fact that it knows that with a 32% market share last year, it is the dominant producer in the market.

Hayat does not issue financial reports, and its references to the Russian market are promotional.

The annual financial reports of Kimberly-Clark do not discuss the Russian market; the last report did acknowledge, however, that Kimberly-Clark is losing ground. “In toilet paper (“consumer tissue”): Net sales in developing and emerging markets decreased 7 percent as unfavorable currency rates reduced sales by about 7 percent.”

Kimberly-Clark spokesmen refuse to answer direct questions about their Russian business, claiming the company doesn’t “share directly” with reporters, though it does with “some reliable market data agencies”. AC Nielsen was recommended by Kimberly-Clark, but the Nielsen office in Moscow refused to answer questions.

The Euromonitor reports fill part of the gap. The Euromonitor analysts also explain that in the Russian market the positions of Essity and Kimberly-Clark have been “constantly challenged by local manufacturers, especially in important categories such as toilet paper. Toilet paper is of the highest necessity and has a strong consumption history in Russia. The distribution of tissue and hygiene in Russia continued towards consolidation in 2018 with no major changes occurring during the review period [2018] or anticipated for the forecast period [2019]. With local consumption shrinking, smaller retailers and even retail chains are forced to fight for survival and each price-sensitive consumer…The negative factors affecting tissue and hygiene during the review period are expected to persist during the forecast period. Consumers’ real income, one of the main preconditions for local consumption development, is set to achieve a low dynamic over the forecast period.”

The Russian toilet paper producers are just as silent; their spokesmen refuse to answer direct questions. They do release partial financial results. Syas Paper and Pulp of Leningrad region, with a 9% market share, leads the domestic producers. It produces these well-known brands, with steadily rising revenues and profits:

SYAS BRANDS

Source: https://syas.ru/

The brand website sources are http://m-znak.ru/ and http://kleo-paper.ru/

SYAS FINANCIAL RESULTS, 2011-2018

Source: https://www.rusprofile.ru/

Syas is not the most profitable of the Russian companies. Syktyvkar of Karelia has reported annual profit of Rb2.3 billion in 2018, five times larger than the Syas profit. Naberezhnye Chelny of Tatarstan says its profit in the same year was Rb1.3 billion; revenue figures are not available. Arkhangelsk Pulp and Paper (Arkhbum) is a leading producer of cellulose but it reveals nothing about its toilet paper production.

According to this report from the timber industry site, LesOnline.ru, at the start of 2018 eight Russian companies claimed to hold a 60% share of the toilet paper market, while Essity was reportedly holding no more than 20%. This is not confirmed by the Euromonitor reports. Another Russian industry source reports that in April 2018, Essity held 14% of the market; Syas 12%; Naberezhnye Chelny, 10%; and Arkhbum 11%.

Sergei Moisiev of Forbes Russia observed in mid-2018 that the market is “an almost an ideal platform for future consolidation. As of 2017, the top five players collectively occupy just over 50% of the market. Thanks to Arkhbum, the number of the top-listed companies will increase to six by 2021. Taking into account the surplus of potential supply, the only options for consolidation with a chance for sustainable and long-term development in future are three or four majors (that is, super-large players).”

Moisiev suggested there are two scenarios for the future. The first would be a takeover by either Essity or Hayat of Russian producers like Syas or Syktyvkar. The second scenario would be the combination of several Russian producers and a concerted effort by their combination to displace Essity, Hayat or Kimberly-Clark from the market.

“The new super-large companies will also have the opportunity to put pressure on the commercial policies of retail chains and suppliers of raw materials, in order to eventually achieve even greater financial privileges for themselves,” Moiseev added.

This is the war now under way on the toilet paper front. It is the reason none of the Russian or foreign producers will agree to talk about their business.

Leave a Reply