By John Helmer, Moscow

Oleg Deripaska (left), chief executive of the Russian state aluminium monopoly Rusal, makes a practice of thriving when everyone else is suffering. That’s because the Russian government and the state banks cast a more protective cover over heavy debtors when times are bad than when times are better.

Rusal owes $9 billion, a sum that has been greater than its stock market capitalization for much of the past year. But since January 1 Rusal’s share price has been doing so well, the company has issued notices to the Hong Kong Stock Exchange claiming it is innocent of any hanky panky. If Deripaska isn’t protesting too much, what then is driving Rusal’s apparent recovery so far this year?

The Rusal board of directors met this week to consider the financial report for the past year. Release of the details followed on Wednesday morning. According to the new report, the cost of producing aluminium was cut in the December quarter by 10.4% to $1,671 per tonne; the London Metal Exchange (LME) price of aluminium has risen in the same period by 11.2% to $1,968; the warehouse premium above LME – a story by itself to be read here – jumped by 53%; and the average sales price of the company’s metal is up 17.3% on the year to $2,419.

In consequence, Rusal’s revenues for the full year 2014 are reported at $9.4 billion; that’s 4.1% less than in 2013. But reported earnings (Ebitda) have leapt by 133% to $1.5 billion. The bottom-line or recurring profit has gone from red to black – from a loss of $598 million in 2013 to a profit of $870 million last year. The Norilsk Nickel dividend which Rusal earns as a 28% stakeholder has grown by 10% to $884 million.

Rusal’s debt currently stands at $9.2 billion. But this year, by arrangement with its creditors, just $255 million is due for repayment. Next year the amount jumps to $1.3 billion. Securing its debts, Deripaska and Rusal have pledged majorities of its large smelter company shares, plus 100% of three offshore entities called Gershvin Investments Corp. Limited (Cyprus), Seledar Holding Corp Limited (Cyprus), and Aktivium Holding B.V. (Netherlands). This troika is the vehicle through which Rusal in Jersey holds its Norilsk Nickel shares. Rusal has promised to bring them into onshore registration in Russia.

In London, comments Andrew Home(right), an aluminium specialist and senior metals columnist for Reuters, “in principle, their profitability should be up on the ruble (affects the Norilsk dividend as well) and lower production costs – they have now closed most of their higher-cost facilities and the result should in theory be a better margin even with the ups and downs in the aluminium price.”

In London, comments Andrew Home(right), an aluminium specialist and senior metals columnist for Reuters, “in principle, their profitability should be up on the ruble (affects the Norilsk dividend as well) and lower production costs – they have now closed most of their higher-cost facilities and the result should in theory be a better margin even with the ups and downs in the aluminium price.”

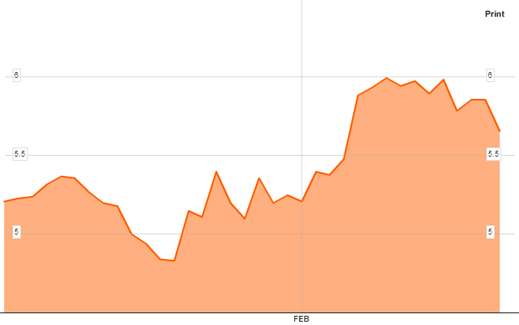

The trajectory of Rusal’s share price in the year to date shows investor optimism was stronger last month, and in the early days of February. It has gone limp this week, as suddenly as it went hard a fortnight ago. In the first hours of trading after the release of the financial report, the share price picked up by 3%, only to fall back again after lunch.

RUSAL SHARE PRICE TRAJECTORY IN THE YEAR TO DATE

Source: http://www.bloomberg.com/quote/486:HK/chart

Comparing other Russian corporations with significant global market share in the non-energy sectors, Rusal is currently (pre-lunch, February 25) 13% ahead on a year-to-date basis, while Norilsk Nickel is presently up 26%; Alrosa, up 17% ; Evraz, up 24%; Novolipetsk Steel, up 18%; and Severstal, up 22%.

Rusal looks better compared to its two global aluminium peers. Alcoa of the US has also had a volatile two months, peaking on February 5, and dropping away this week. At today’s share price, Alcoa is down 7.5% in the year to date.

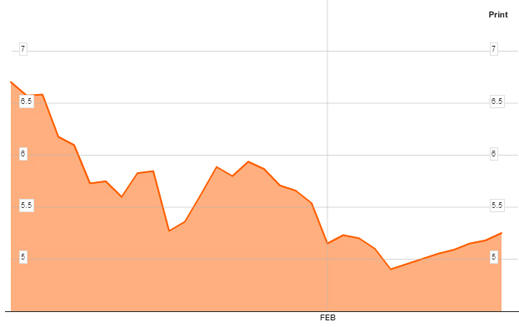

The Aluminium Corporation of China (Chalco) enjoyed a burst of share price growth late last year, hitting peak on January 5. It’s down 26% since then. Chalco has been loss-making, and corruption investigations by the Chinese authorities haven’t helped encourage stockmarket demand. Once it became clear that Chalco’s 2014 loss would be bigger than expected, its share price gain became unsustainable.

CHALCO SHARE PRICE TRAJECTORY IN THE YEAR TO DATE

Source: http://www.bloomberg.com/quote/601600:CH/chart

On January 30, Rusal issued operating results for the December quarter and for the full year of 2014. The press release claimed there had been “a marked turnaround in the aluminium market. Thanks to production cuts as well as a continued increase in demand, the 2014 ex-China market ended in deficit, supporting the LME price and also regional premiums.” Aluminium output fell to 3.6 million tonnes (annual), down 7% compared to 2013. Production of alumina, the feedstock for the metal smelters, was down 1% to 7.3 million tonnes. Bauxite output, the raw material for alumina, was 12.1 million tonnes, up 2% on the year, but with a decided reduction in the final quarter.

The company has eliminated aluminium production almost entirely in western Russia. The Volkhov (Leningrad region), Bogoslovsk (Sverdlovsk), and Uralsk (Sverdlovsk) smelters have been halted altogether. Nadvoitsk (Karelia) and Novokuznetsk (Kemerovo) have been cut by 60%; Kandalaksha (Murmansk) by 2%. The older, hydropower-fuelled smelters in the east – Bratsk, Krasnoyarsk and Sayanogorsk – have been operating at year-before levels, while output at the newest Siberian smelters – Taishet and Khakas – are up in volume by single digits. The smelters which are closed are going to stay closed, the company reports.

According to Rusal’s assessment, the rising price of commodity aluminium, and the continuing gain in premiums paid for the metal, demonstrate strengthening market demand and the financial improvement the company is hoping for this year. “While RUSAL expects stable aluminium production volumes and favorable pricing environment in 2015, the Company does not plan to restart the aluminium smelters idled in 2013/2014 due to the current market environment so to maintain production discipline… we estimate that an increased usage of aluminium across a wide range of sectors will mean that demand for the metal will grow by 6.5% in 2015.”

In Rusal’s report to the market today, “with the ramifications of the 2009 industry crisis firmly in our mindset, the Company has no plans to restart any mothballed aluminium capacity, regardless of the LME price.”

Even if the forecast growth of demand doesn’t materialize, there are domestic Russian factors weighing in Rusal’s favour. Deripaska hasn’t been sanctioned by the US or European Union (EU) yet, although his right to cross the US frontier isn’t exactly unrestricted. For that story, click. Deripaska has been careful to toe the Kremlin’s anti-US line without committing himself too explicitly on Crimea or Novorussia.

This week all that Rusal has to say about the war next door, and its ramifications at home, is: “The recent conflict in Ukraine and related events has increased the perceived risks of doing business in the Russian Federation. The imposition of economic sanctions on Russian individuals and legal entities by the European Union, the United States of America, Japan, Canada, Australia and others, as well as retaliatory sanctions imposed by the Russian government, has resulted in increased economic uncertainty including more volatile equity markets, a depreciation of the Russian Ruble, a reduction in both local and foreign direct investment inflows and a significant tightening in the availability of credit. The longer term effects of recently implemented sanctions, as well as the threat of additional future sanctions, are difficult to determine.”

Like Roman Abramovich’s Evraz, Deripaska’s (below, right) Rusal is one of the most heavily indebted Russian companies in relation to its earnings (Ebitda). Like Abramovich (left) too, Kremlin sources believe President Vladimir Putin’s personal relationship with the two is reinforced now by the political role they play in preserving employment at their plants around the country. This, the sources add, “was just as obvious during the crisis of 2008 and 2009.”

“In the current Russian crisis,” one of the sources says, “it is safe to conclude that the state will protect its strategic corporations from the pressure from debt-holders among the state banks. The rising price of oil translates into a more stable budgetary position for the state, and also for the state banks.”

Can this confidence have motivated the burst in Rusal’s recent stock price?

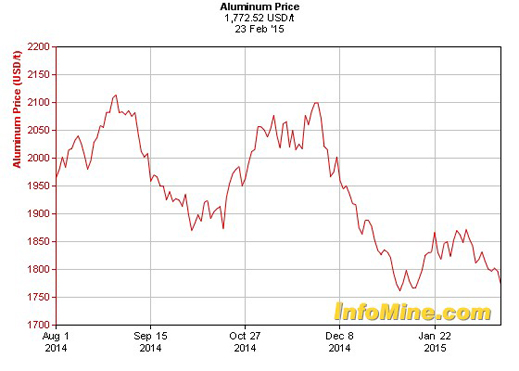

A Swiss aluminium trader suggests this is nothing more than short-term speculation. “Rusal is not a transparent company, and it’s difficult to know who are the buyers and sellers on the stock exchange for Rusal shares in Hong Kong. Under the present circumstances, it does not make sense to consider the Rusal share for investment purposes, but only for speculation. But who are the speculators? For them, the aluminium price on the present level has no significance regarding the share price.”

THE SIX-MONTH TRAJECTORY OF THE LME ALUMINIUM PRICE

Source: http://www.infomine.com

Rusal has been concerned enough by the matter of who is speculating on its shares to have issued two notices to the Hong Kong exchange, one on February 6, and a second four days later. In the first notice, the company claimed: “The board of directors (the “Board”) of United Company RUSAL Plc … has noted the recent increases in the price and the trading volume of the shares of the Company on 5 February 2015. Having made such enquiry with respect to the Company as is reasonable in the circumstances, the Board confirms that it is not aware of any reasons for these price and trading volume movements of the shares of the Company or of any information which must be announced to avoid a false market in the Company’s securities or of any inside information that needs to be disclosed under Part XIVA of the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong).”

The language of the second notice was the same, including the qualifier of “such enquiry as is reasonable in the circumstances.” It is noteworthy that when Rusal’s share price last breached the HK$6 threshold – in February 2012 and in November 2014 – the company issued no disclaimers of inside trading.

What is missing from the good news bulletins, and especially from the Ukraine war-risk notice in today’s financial report, is the threat that Rusal has been facing for a year that its Russian smelters might lose alumina feedstock from the Nikolaev Alumina Refinery (NGZ), in southeastern Ukraine.

Nikolaev is 600 kilometres to the southwest of Donetsk. From Nikolaev, if you drive eastwards on Route E58, it will take about six and half hours before you come within range of the artillery and rocket batteries along the current line of contact between the Novorussian forces and the Ukrainian Army dug in around Mariupol.

Since the start of the Ukrainian civil war in the Donbass, Rusal has been reporting no problems at the Nikolaev refinery in what Deripaska called “the safe zone in the south”. For example, see this. The full-year production reports by Rusal and the refinery indicate as much: in the December quarter NGZ produced 371,000 tonnes of alumina, an increase of 5% over the September quarter. For the full year of 2014, refinery output was 1.46 million tonnes, 45,000 tonnes or 3% less than the year before.

Altogether, at refineries in Ukraine, Ireland, Australia, Russia and Jamaica, Rusal says it is producing 7.3 million tonnes of alumina per year. For Rusal’s Russian smelters, NGZ produces one tonne in five of their feedstock requirement.

This week in Kiev the Ukrainian government’s privatization agency, the State Property Fund, confirms that it continues to pursue Rusal with court action to cancel its leases on the five berths at Dnieper-Bug Port, in the Bug River Estuary (pictured below). These are the facilities on which the refinery depends for incoming bauxite to refine. NGZ’s outgoing alumina for delivery to Rusal’s smelters in Russia reportedly goes to Russia by train.

Rusal’s position is that this Ukrainian government challenge has been beaten off; the court litigation in Kiev is over; and that Rusal has successfully renewed its Dnieper-Bug berth leases for another fifteen years.

According to the refinery, in a recent press release to local Ukrainian media, in 2014 NGZ upped its worker wages by an average of almost 16%. The plant claims to be one of the largest taxpayers in its region, and to have increased tax payments in 2014 by 38% over the previous year. Last year NGZ says it paid UAH340 million in municipal, regional and state taxes. This local press report was published on February 3. It claims Rusal has finalized a 15-year extension of its leasehold at Dnieper-Bug port.

What happened, according to sources in Kiev and to this Ukrainian press report, is that when Rusal took full ownership of the refinery in a privatization deal with the Ukrainian government, it wanted to buy the Dnieper-Bug port facilities as well. The government did not agree, however, and the berths have been leased on a 15-year term. That ran out on April 1, 2014. Rusal asked for a full 15-year renewal. The government in Kiev, including the privatization agency, the Ministry of Infrastructure which is responsible for ports, the Ministry of Transport, and the Ministry of Economy offered a 3-year term with a substantial increase in the rent. That had been UAH11 million per annum.

What happened, according to sources in Kiev and to this Ukrainian press report, is that when Rusal took full ownership of the refinery in a privatization deal with the Ukrainian government, it wanted to buy the Dnieper-Bug port facilities as well. The government did not agree, however, and the berths have been leased on a 15-year term. That ran out on April 1, 2014. Rusal asked for a full 15-year renewal. The government in Kiev, including the privatization agency, the Ministry of Infrastructure which is responsible for ports, the Ministry of Transport, and the Ministry of Economy offered a 3-year term with a substantial increase in the rent. That had been UAH11 million per annum.

To prevent the government reclaiming the port assets Rusal went to court in Kiev, demanding renewal of the expired lease on the same terms. In June Rusal won an injunction from the court blocking any action by the government to seize the port and oust the pro-Rusal management. In August the Kiev court ruled in favour of Rusal’s lease renewal claim. In October, and then again on December 23, Rusal’s lawyers won judgements rejecting the government’s appeals. A final appeal is now being considered, government officials said this week.

Russian maritime reporters admit they have known nothing of the fight over the Dnieper-Bug leases. There has been no Russian press coverage of the threat to Rusal. In the Ukraine, none of the anti-Russian media has noticed the court battle between the government and the Russian-owned plant. TThe Nikolaev region media reports have failed to reach the market; Rusal has not disclosed to shareholders or to the Hong Kong Stock Exchange that there has been any risk in the litigation.

This week’s report by Rusal on its current legal provisions says: “The Group’s subsidiaries are subject to a variety of lawsuits and claims in the ordinary course of its business. As at 31 December 2014, there were several claims filed against the Group’s subsidiaries contesting breaches of contract terms and non-payment of existing obligations.” In the latest report of “legal contingencies”, Rusal refers to a well-known court case in Nigeria, but ignores the proceedings in Ukraine. Throughout last year’s litigation in Kiev, Rusal’s management and board shielded the Rusal share price from an evident threat to the company’s operations and chain of production.

What then, in addition to this subterfuge, has been driving the Rusal share price, but keeping it from crossing the HK$6 threshold? “My suspicion,” says Pani Klikis, a London aluminium trader for Minimet, Mitsui, Trafigura and now LN Metals, “is that there is nothing magical about the [HK] $6 price level, probably [it’s] just an old resistance area. Considering that the aluminium price is a little lower than 2012, the [share] price increase has more to do with the increase in the premium (which has more than doubled over the past two years) and the perceived future strength of the aluminium market.”

“Aluminium is a very efficient way of exporting energy. Thus, the production costs of Rusal, in view of lower oil and gas [prices], must be much lower than they have been in a long time. The run-up of the share price I would say is justified. Also, the final aluminium price (delivered works) has decoupled from the LME outright price; investors may have finally realised that there is a physical element to the aluminium price, at these levels making up 1/4 to 1/2 of the total final price, which until recently had not been taken in to account by investors.”

There is speculation in the market, according to Klikis, that if Rusal’s share price can be ramped up above the six-dollar level, there may be a fresh attempt by Deripaska to raise the value of Rusal in relation to Norilsk Nickel, and attempt another reverse takeover. For the end of his abortive attempt in 2012, read this.

How do sources in Nikolaev and close to Rusal in Moscow explain the readiness of the Russia-hating government in Kiev to allow Deripaska to win in court over the State Property Fund? Ukrainian sources say the alumina refinery is so important to the city and region, there is reluctance in Kiev to upset the economic order for fear of provoking fresh separatist protests and Novorussian movements further southward.

A Ukrainian source close to NGZ explains there is no Ukrainian raider who wants to take the refinery from Deripaska, since if NGZ were taken from him, Deripaska could then retaliate by cutting off the supply of bauxite from Rusal’s mines in Guinea. A Ukrainian raider would also be beholden to Rusal for smelters to consume the alumina. The source believes government officials want to lift the state rent at Dnieper-Bug, and also their take. “If they [Ukrainians] had wanted, they would have taken [the asset]. And so it seems that [what they really wanted] is additional income for the officials.”

In Moscow, one source close to Rusal responds: “If you are looking for the link [between Deripaska] and [Prime Minister Arseny] Yatseniuk, ask Glencore.”

Leave a Reply