By John Helmer, Moscow

Officials of the International Monetary Fund (IMF) are in flight from evidence of negligence, incompetence, and corruption in their management of billions of dollars in loans for Ukraine.

Nikolai Gueorguiev, head of the Ukraine team at IMF headquarters in Washington, DC, and Jerome Vacher, the IMF representative in Kiev, refuse to respond to questions on their role in the offshore diversion of IMF loan money through Privatbank and Credit Dnepr Bank, banks owned by Ukrainian oligarchs Igor Kolomoisky and Victor Pinchuk. The Fund’s Managing Director Christine Lagarde (lead image, front) and her spokesman, Gerry Rice (rear), are covering up evidence of conflicts of interest and multiple violations of the IMF Staff Code of Conduct which have been occurring in the Ukraine loan programme. Simonetta Nardin, head of the Fund’s media relations, refuses to explain her apparent violations of the Code, or respond to evidence that she fabricated elements of her career resume.

On Tuesday a spokesman at the US Department of Justice in Washington confirmed that an investigation is under way of the role played by US clearing banks in the movement of IMF funds through the Privatbank group and companies connected with Kolomoisky. Speaking for the Asset Forefeiture and Money Laundering Section, Peter Carr declined to give more details.

In recent indictments presented to US courts, Justice Department officials have defined the crime of money laundering as the transmission or transfer of money through “a place in the United States to or through a place outside the United States” with the “intent to promote the carrying on of specified unlawful activity”; with knowledge that the transfer of funds represents “the proceeds of some unlawful activity”; and with the intention to “conceal or disguise the nature, the location, the source, the ownership, or the control of the proceeds of unspecified unlawful activity”.

The role of US system banks, such as Citibank, Bank of America, and JPMorgan Chase, in clearing US dollar transactions has been the basis of selective Justice Department prosecutions of Russian and pro-Russian Ukrainian companies and individuals since the toppling of President Victor Yanukovich in Kiev in February 2014. In contrast, Ukrainian allies of the US in that operation, including Yulia Tymoshenko (below, left), Kolomoisky (centre), and Pinchuk (right), have not been pursued on court evidence of their involvement in corruption and money-laundering.

Washington’s selectivity and political favouritism was condemned by an Austrian court in May, when a US extradition request for Dmitry Firtash on corruption charges was rejected. Justice Department lawyers are now attempting a retrial of their allegations in an appeals court in Vienna.

For the Justice Department to acknowledge this week that it is investigating Kolomoisky is unusual. Kolomoisky himself was last recorded as visiting the US in April; follow that story here. He is based in Geneva, where a Swiss Government investigation of his qualification for renewal of a residency permit continues without end.

For the US to acknowledge opening an investigation of IMF lending to Ukraine is unprecedented. The IMF resumed its loan disbursements to Ukraine in March. This was after a hiatus of six months from October of 2014, when the Stand-By Arrangement (SBA) agreed the previous April was suspended as Fund officials attempted to convince the board that the Kiev government was capable of repaying its debts and meeting its loan conditions. When the Fund launched the SBA on April 30, 2014, it had claimed: “A strong and comprehensive structural reform package is critical to reduce corruption…to build capacity to more effectively conduct enforcement of anti-money laundering and anti-corruption legislation.”

The IMF reports that in 2014 it gave $2.2 billion to the National Bank of Ukraine (NBU) before the suspension. Another $5.4 billion in IMF cash was paid to Kiev for what is called “budget support”. That also included warfighting in eastern Ukraine.

When the IMF board agreed to restart lending with a new arrangement called the Extended Fund Facility (EFF), the American deputy managing director of the Fund, David Lipton, claimed: “Restoring a sound banking system is key for economic recovery. To this end, the strategy to strengthen banks through recapitalization, reduction of related-party lending, and resolution of impaired assets should be implemented decisively.” Using the future tense Lipton (below, left) was acknowledging that next to nothing had been done to reform the Ukrainian banks in fifteen months.

Gueorguiev (right), an ex-official of the Bulgarian government, has claimed he is in charge of the independent auditing and supervision of the Ukrainian banks; for the record of his admissions in June 2014, click. Since then Gueorguiev refuses to answer questions.

In the new staff report for which he and Jerome Vacher, the IMF resident representative in Kiev, are responsible, issued a month ago, they admitted the condition of the Ukrainian banks is parlous. “Outstanding NBU loans are still elevated for a number of domestic banks. At end-June, the aggregate liquidity ratio among the 35 largest banks was 15.2 percent, although seven of these domestic privately-owned banks had liquidity ratios below 5 percent.” Privat and Credit Dnepr, the Kolomoisky and Pinchuk pocket banks, aren’t identified.

Gueorguiev omits to note that the current liquidity measure for the Ukrainian banks is several points worse than it was at the start of this year. His report does reveal that the banks’ non-performing loan (NPL) ratio and their capital adequacy ratio (CAR) have deteriorated while Gueorguiev has been in charge. In June 2014 the CAR was 15.9%; in January 2015, 13.8%; at the start of this past June, 7.7%.

That ought to have flagged the question of where the money the IMF was putting into the Ukrainian banks has gone, if men like Lifton, Gueorguiev and Vacher, and Mrs Lagarde, have been unable to staunch the haemorrhaging of their clients’ liquidity. In March, when the IMF released $4.6 billion of new EFF money, they also approved the NBU issue of more cash to Privatbank “to ensure timely implementation of… PrivatBank’s obligations to depositors…[and] to support its liquidity.”. Click for this story.

Gueorguiev and his staff reported in August to Lagarde and the board that “the top 10 banks submitted reports on related party exposure based on the new legal and regulatory framework by mid-June and a review process by independent accounting firms has begun. Once this is completed, the next stage—unwinding the above-the-limit loans to related parties––will commence. Additionally, the authorities are also working on the establishment of a specialized unit that will identify and monitor loans to related parties in all banks.”

Gueorguiev was reiterating a promise to do in future what he had promised, and failed to do, since June of 2014. He and the Fund management are now claiming they plan to help “the NBU’s monitoring capacity through greater information sharing with public registers and other financial sector regulators on shareholdings and asset ownership.”

“A new wave of bank diagnostics, based on data as of March 2015, is underway,” Gueorguiev is now proposing, “with the aim to identify capital shortages as a result of losses associated with the recent macroeconomic shocks and the ongoing conflict in the East.” Privatbank isn’t mentioned in the report, but as it is the leading commercially-owned systemically important bank (SIB) in the Ukraine, when the IMF reports refer to SIBs, they mean Privat.

The new staff report claims it has been decided to continue making “provision related loans in full and transfer them into a specialized unit inside the bank in case it is needed to ensure medium-term financial viability of any resolved SIB. [And] inject public funds in the SIBs only after shareholders have been completely diluted and non-deposit unsecured creditors are bailed in.” This looks like the IMF has decided to oust Kolomoisky from control of Privatbank. It may be advance warning for him to empty the bank’s pockets into his own before the dilution and other conditions take effect. That would make Gueorguiev and his IMF colleagues complicit in the money laundering schemes the Justice Department is investigating – if evidence turns up that they knew, or ought to have known, of transfer schemes intended to defraud the bank, its collateral shareholder NBU and lender IMF, by hiding the cash offshore under Kolomoisky’s personal control.

This week Gueorguiev was asked to start with data which are missing from the staff report. What is the current aggregate of IMF provision of ELA [emergency liquidity assistance] and other funds to the NBU for 2014 and 2015 through August 31? he was asked. What does the IMF understand to have been the receipt (to current date) of NBU funds by Privatbank and Credit Dnepr Bank? These ought to be uncontroversial data, required for disclosure according to what the IMF terms its transparency and governance standards in Ukraine.

Independent Ukrainian bank publications indicate that at the start of June the NBU and the associated Deposit Guarantee Fund (DGF) had loaned 131.9 billion hryvnia (UAH) to the commercial banks for liquidity support. That’s about $6.3 billion at the current dollar-hryvnia rate of exchange, all of it from the IMF. On last year’s evidence, Privatbank’s systemic importance enabled it to garner about 40% of this outlay, making about $2.5 billion.

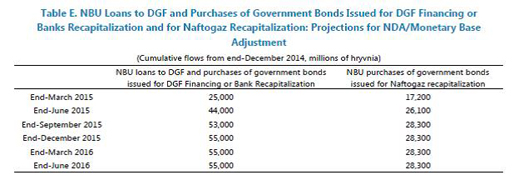

Since the start of June, however, the IMF has given Kiev another $1.7 billion. How much of that has gone, or will go, into emergency liquidity assistance for the NBU and DGF, and how much has been moved on to Privatbank are sensitive secrets. A table in one of the technical papers attached to the IMF’s latest report indicates that between the end of June and the end of this month, the IMF is figuring the NBU will pass on about $410 million of the new money. That would make $164 million for Privatbank if it is still absorbing 40% of the total outlay.

Source: http://www.imf.org -- page 86

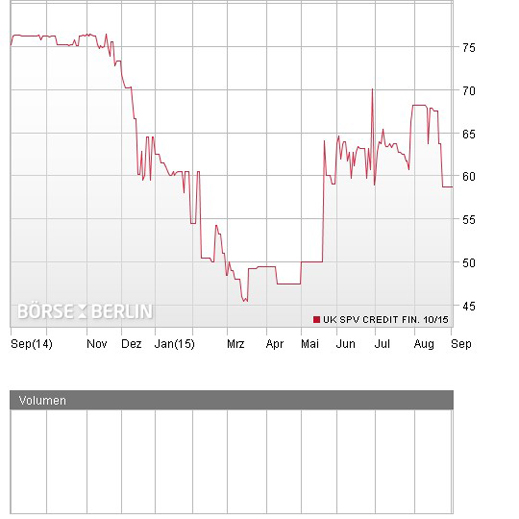

More public is Privatbank’s claim to be currently unable to repay its foreign creditors. According to this report of July 24, the bank is required to redeem a $200 million bond issue later this month, but cannot make the repayment. If it defaults, another $150 million bond, due for redemption next year, would be called in. Foreign bondholders think the bank has the cash to repay. Privat officials claim they have been ordered by the government to cover domestic depositors first, and defer other obligations by getting deferment agreements for several more years. Follow Privat’s version of the bond deferment scheme here. The impact has been to halve the trading value of the 2015 bond:

Source: http://www.boerse-berlin.com

Rating agency Moody’s is currently warning that the rot in the Ukrainian banks will get worse, not better, despite the fresh IMF money supply. “System-wide problem loans could rise to as much as 60% of gross credit exposure from 45% at the end of 1 April 2015,” says Elena Redko, a Moody’s analyst and author of this report. “Our scenario analysis indicates that banks would need to create additional loan-loss provisions of 15% of gross loans, on top of already existing loan loss provisions, in order to fully cover expected losses. If applied, incremental provisioning would result in a negative capital adequacy ratio for the banking system,” she added. Moody’s has issued a private warning on Privatbank.

Privatbank was asked to say how much it has received in liquidity assistance from the IMF programme. It refuses to say.

Gueorguiev has been asked what happened to the fish that got away. “How do you explain that while you were supervising the disbursement of IMF funds through the NBU to the Ukrainian banks, assessing the NBU’s regular reports and assessing loan compliance for your superiors, it was possible for Privatbank to divert at least $1.8 billion now recognized in the Ukrainian courts to be in default? What do you say in defending yourself from the charge, naturally arising now, that you are personally culpable, by intention or by carelessness, for the Privatbank violations identified in the court evidence? ” Gueorguiev isn’t claiming the constitutional right not to incriminate himself. He isn’t defending himself either.

The evidence of the disappearance of $1.8 billion has emerged in commercial court filings in Dniepropetrovsk, Kiev and elsewhere by the Privatbank group itself as recovery claims against purportedly unrelated borrowers who have defaulted. That, according to independent Ukrainian investigations, is in fact a massive fraud scheme, in which the money was loaned to related parties, deposited in offshore Privatbank accounts, before disappearing altogether. Privatbank has issued a press release, claiming the non-performing loans are genuine ones, not thefts. “We are convinced that the investigation by examining the documents to which access was granted by the court will be able to objectively assess all the circumstances together, and to establish the truth,” the bank said.

Several English-language reporters have investigated the disappearance of the $1.8 billion, starting with Graham Stack (right) in Kiev. A selection of the offshore entities and amounts involved can be followed in this Ukrainian report. A few days ago in the US magazine Harper’s, a reporter named Andrew Cockburn took credit for uncovering the story himself.

Several English-language reporters have investigated the disappearance of the $1.8 billion, starting with Graham Stack (right) in Kiev. A selection of the offshore entities and amounts involved can be followed in this Ukrainian report. A few days ago in the US magazine Harper’s, a reporter named Andrew Cockburn took credit for uncovering the story himself.

In New York this week, an international banker said the publicity is confirmation of what was already known. His colleagues all understand, the source said, the extent to which IMF officials, including Lipton and his US Treasury associates, have winked at the stealing of Fund loan money by Ukrainian figures who are allies of the US-appointed officials now running the country. “It’s no news the stealing continues. But once the evidence moves into court, and then into the American press, it isn’t the Ukrainian thieves who are on the hot seat. It’s those American, British, and European nationals in charge of the cover-up, whose liability becomes actionable. How long can Lagarde and Lipton carry risks like that?”

Even the Russia-haters in Kiev publicly concede that official corruption is undiminished. Andriy Parubiy, ex-head of the Defense and National Security Council, as the President’s war office is known, recently lost out in faction-fighting over the flows of arms and money; he blames the rampant corruption – on his rivals. Parubiy (below, left) is keeping his post as Vice-Speaker of the Verkhovna Rada (parliament). Late last week, he proposed a US Department of Justice official, Mary Butler (right), for a post on the government’s Select Commission on Anti-Corruption Prosecutor.

Butler has been the Justice Department’s representative in Kiev; at present she is Deputy Chief of the Asset Forfeiture and Money Laundering Section at headquarters. Her involvement in pursuit of Firtash and the Russian telecommunications companies Vimpelcom and MTS has been reported here. When Department spokesman Carr admitted this week that an investigation of Privatbank and Kolomoisky is underway, he was asked to clarify the details with Butler. She and the spokesman aren’t saying more.

Vacher (right), the Fund’s resident representative in Kiev, may be of greater interest to US investigators because he appears to have been exchanging valuable favours with Pinchuk. Questioned about his trip to Venice in May to attend a Pinchuk art show and political rally, Vacher is admitting through the Fund’s press office that he wasn’t on official duty at the time. But did he stay on board Pinchuk’s motor yacht Oneness, which port logs show to have been in Venice between May 4 and May 8? Vacher and his superiors in Washington are withholding their answer. For more details of Vacher’s relationship with Pinchuk, read this. For the impact of the IMF loan programme on Credit Dnepr Bank, click here.

Vacher (right), the Fund’s resident representative in Kiev, may be of greater interest to US investigators because he appears to have been exchanging valuable favours with Pinchuk. Questioned about his trip to Venice in May to attend a Pinchuk art show and political rally, Vacher is admitting through the Fund’s press office that he wasn’t on official duty at the time. But did he stay on board Pinchuk’s motor yacht Oneness, which port logs show to have been in Venice between May 4 and May 8? Vacher and his superiors in Washington are withholding their answer. For more details of Vacher’s relationship with Pinchuk, read this. For the impact of the IMF loan programme on Credit Dnepr Bank, click here.

Reporting to Managing Director Lagarde as chief spokesmen for the Fund’s Ukraine operations are Rice, a British national, and Simonetta Nardin, an Italian. She claims to have been a journalist in Italy before joining the IMF in 1997. In a forum sponsored by the US Government’s National Endowment for Democracy, the Czech Foreign Ministry, the European Commission, and a Taiwan government office in Prague, she also claimed her role is “to make the IMF responsible and accountable for what it does.”

Nardin is ducking questions about Vacher’s political demonstration for Ukrainian causes funded by Pinchuk. She and Rice have also avoided questioning about Nardin’s own involvement in political demonstrations she has published on the internet in favour of President Barack Obama and the Democratic Party presidential candidate, Senator Elizabeth Warren. The IMF Staff Code forbids this.

Source: http://picasaweb.google.com

Nardin (above, left) says she studied at universities in Milan and London. Between 1994 and joining the IMF press office in 1997, Nardin claims she was a journalist in Italy. The Italian guild of journalists (Ordine dei Giornalisti) recorded her membership for the Lazio region (Rome) in October 1998. By that time she had been serving at the IMF for eighteen months. There is no sign that she had published as a reporter to qualify for guild membership; no record of her byline has been found in Milan and Rome. When asked last month to provide the evidence for her claim, Nardin refused.

As soon as she was asked, Nardin’s biography was removed from the IMF website. What remains is the record from last December, when Rice promoted her to be chief of his Media Relations Division. Reporters at a Fund briefing were obliged to clap their hands. “I would like to give a quick round of applause to Simonetta,” announced the briefer, “because she deserves this appointment. For those of you who do not know Simonetta it’s important that you get to know her. So I look forward to hearing more from you in the future.”

Leave a Reply